The End of Blockchains? 7 Ways Networks Actually Die (And How to Spot the Warning Signs Early)

“Blockchains are unstoppable” is one of crypto’s favorite slogans. It sounds plausible until you ask a more useful question: unstoppable in what sense? A network can keep producing blocks while losing the things users, developers, and investors actually care about.

That is usually how blockchains die. Not through one dramatic shutdown, but through gradual decay. Security weakens. Governance gets captured. Bridges turn into systemic liabilities. Developers stop showing up. Liquidity leaves. Price often reacts late.

So the better question is not whether blockchains can end. It is how they fail in practice, and which signals tend to appear before the market fully notices. Once you look at chains this way, the pattern becomes clearer: most failures cluster around a small set of recurring risks.

This article maps seven of them and ends with a simple resilience checklist you can use across L1s, L2s, rollups, and appchains.

What it means for a blockchain to “die”

Death is usually functional, not literal

A blockchain does not need to disappear to be effectively dead. It can stay online while losing security, liquidity, credible neutrality, developer attention, or user trust.

That distinction matters because many people still watch the wrong indicators. If blocks keep coming and the token still trades, the chain looks alive. But block production is a very low bar. What users came for was something more valuable: reliable settlement, resistance to capture, usable liquidity, and a reason to build there.

A chain that still runs but no longer secures meaningful value, attracts builders, or offers neutral rules is not healthy. It is just lingering.

A chain can survive technically and still fail economically

This is common in crypto’s quieter failures. Some chains do not implode. They fade into irrelevance. Others remain online but depend on one bridge, one sequencer, one stablecoin issuer, or one foundation multisig to keep functioning.

That is why “death” is best understood as losing the properties that made the network valuable in the first place. In practice, that often means one or more of these:

- security no longer matches the value being secured

- rules are no longer credibly neutral

- liquidity becomes fragile or fragmented

- critical infrastructure can be pressured off-chain

- users and developers gradually stop caring

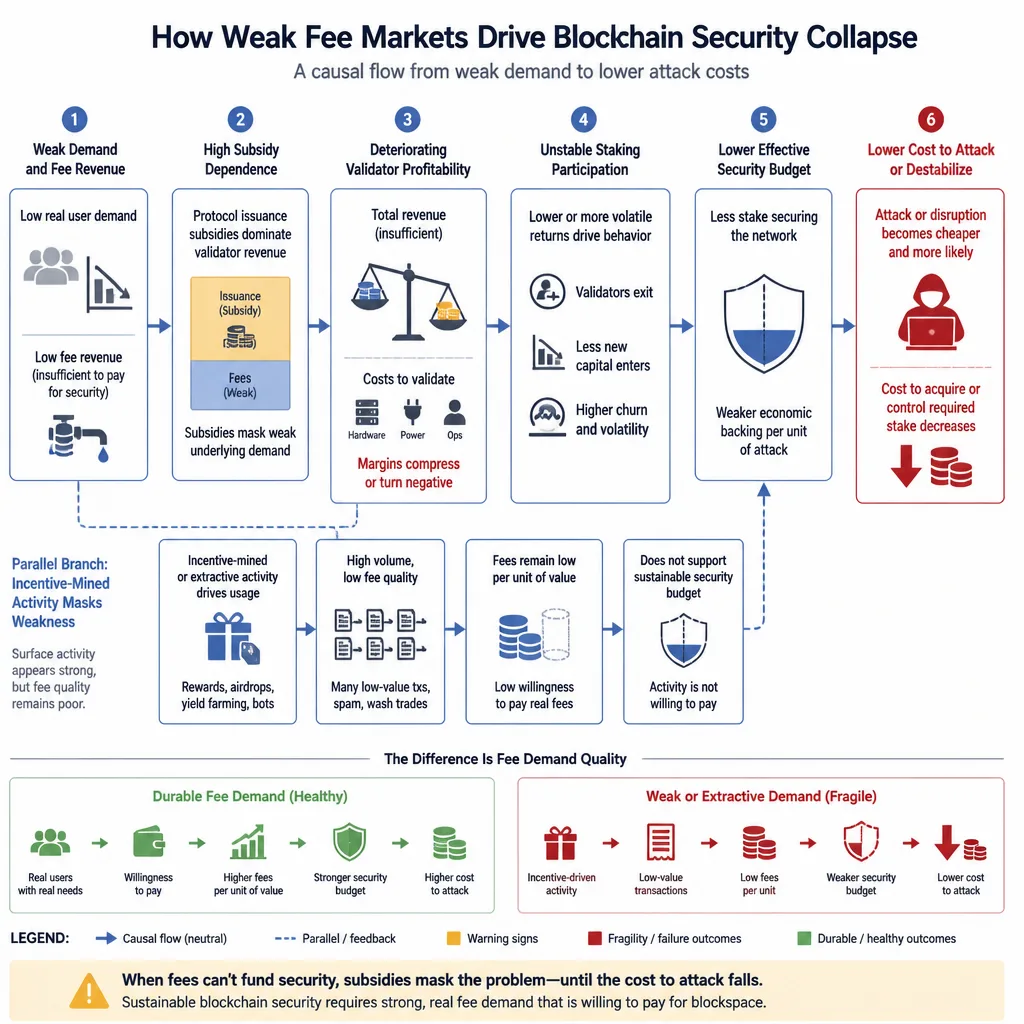

1. Security collapse when the fee market cannot support the chain

Low activity is not just a growth problem

Security is not abstract. It has to be funded.

In proof-of-work, that means enough reward to sustain hashpower and keep attacks expensive. In proof-of-stake, it means validator incentives must remain strong enough that the network is costly to corrupt and worth participating in. In rollups and appchains, you also need to separate execution activity from the security that is inherited or purchased elsewhere.

The common mistake is treating low usage as only a demand problem. Often it is a security problem. If a chain’s real fee revenue is weak, the cost to attack or destabilize it may be lower than the market assumes.

Subsidies can hide a weak security budget

Emissions can make sense early. Bootstrapping a network is not the same as failing. But there is a difference between temporary support and a model that never matures.

A chain can look healthy because it pays users, liquidity providers, validators, and apps to stay. That can obscure a simpler reality: the network is not earning its security. It is renting it.

This matters most when token prices are still strong. Price can mask a weak security budget for a while. But if fees stay low, issuance becomes harder to justify, or validator economics deteriorate, the underlying fragility shows up fast.

Warning signs

Watch for:

- declining real fee revenue

- a wide gap between issuance and organic fees

- falling validator or miner profitability

- unstable staking participation or sudden yield shifts

- obvious incentive-mined activity with little durable demand

A useful check: if incentives vanished next quarter, would meaningful users still be there?

2. Governance capture that breaks credible neutrality

Governance can become a control surface

On-chain governance sounds democratic. Sometimes it is. Sometimes it simply makes capture easier to observe.

A blockchain becomes less valuable when users believe important rules can be changed by insiders, large token holders, foundations, validator cartels, or emergency committees with little resistance. That is what breaks credible neutrality: the idea that rules apply consistently rather than selectively.

For developers, this is not abstract. If you are building a serious application, you want to know whether the platform’s economic rules, censorship posture, or upgrade path can be rewritten in a political rush.

Capture usually looks ordinary, not dramatic

It rarely appears as one obvious takeover. More often it emerges through low turnout, delegated apathy, treasury dependence, or off-chain coordination. The vote happens on-chain, but the real decision was made elsewhere.

Even high participation is not always reassuring. In some ecosystems, it reflects recurring rent-seeking rather than broad legitimacy.

Warning signs

Look for:

- concentrated voting power

- low-turnout proposals with high stakes

- rushed governance timelines

- repeated use of emergency powers or multisigs

- major decisions effectively pre-coordinated off-chain

A practical question helps here: who can change the rules in practice, not just in theory?

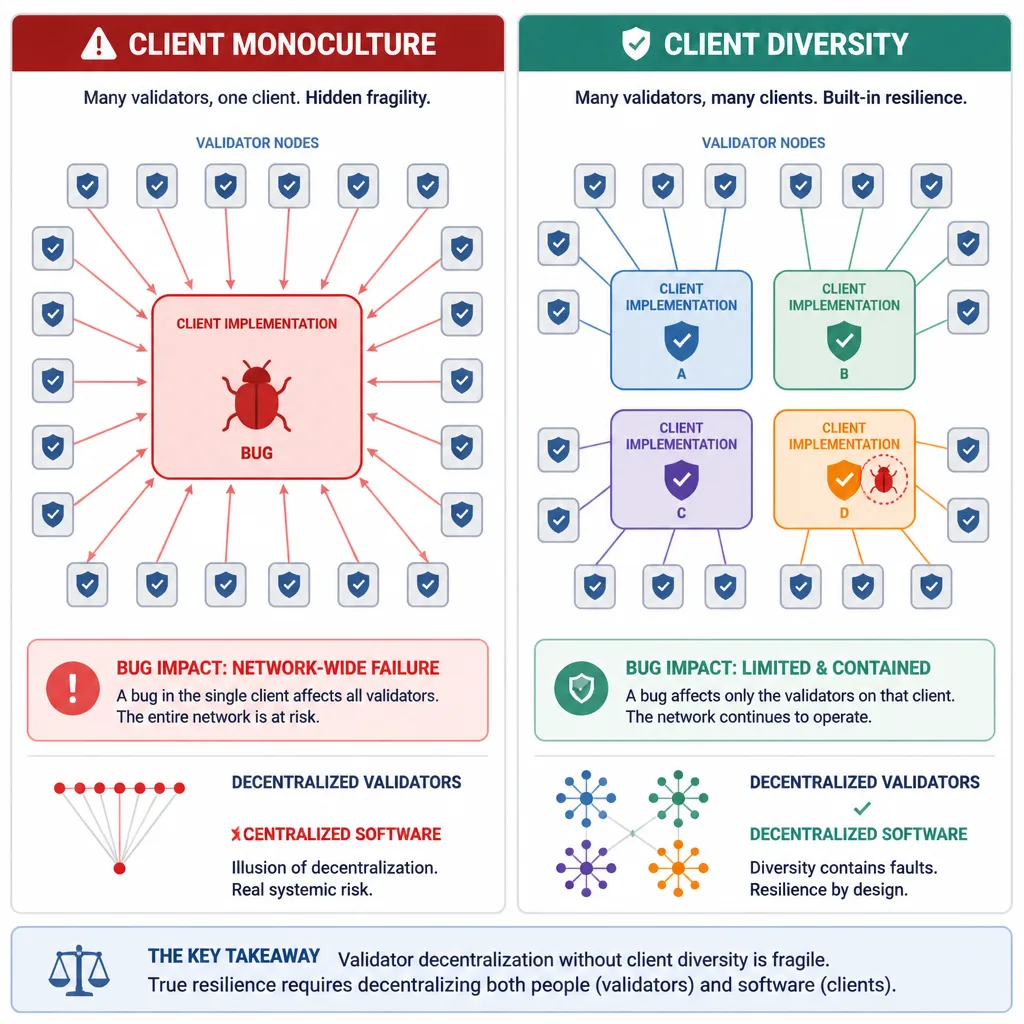

3. Client monoculture and the single-bug failure problem

Software diversity matters more than it seems

Validator decentralization can be undermined by software centralization.

If most of a network runs one client implementation, one critical bug can become a network-wide incident. That is true even if thousands of validators appear independent on paper. If they all rely on the same code path, they can fail together.

Ethereum’s emphasis on client diversity exists for this reason. The same issue applies across L1s, and increasingly across rollup stacks that depend on shared codebases.

One dominant client can turn a bug into a systemic outage

This is the kind of risk the market tends to underprice because it feels too technical until it becomes real. A malformed block, consensus bug, or bad patch can create correlated failure across operators that look independent.

Many operators do not create real resilience if they all run the same client, use the same cloud setup, and depend on the same small team for fixes.

Warning signs

Monitor:

- one client dominating validator share

- weak maintenance of minority clients

- poor testnet diversity

- slow or fragile incident response

- dependence on one upstream vendor or repo

A rough rule: if one implementation failing would impair most of the network, the chain is less decentralized than it looks.

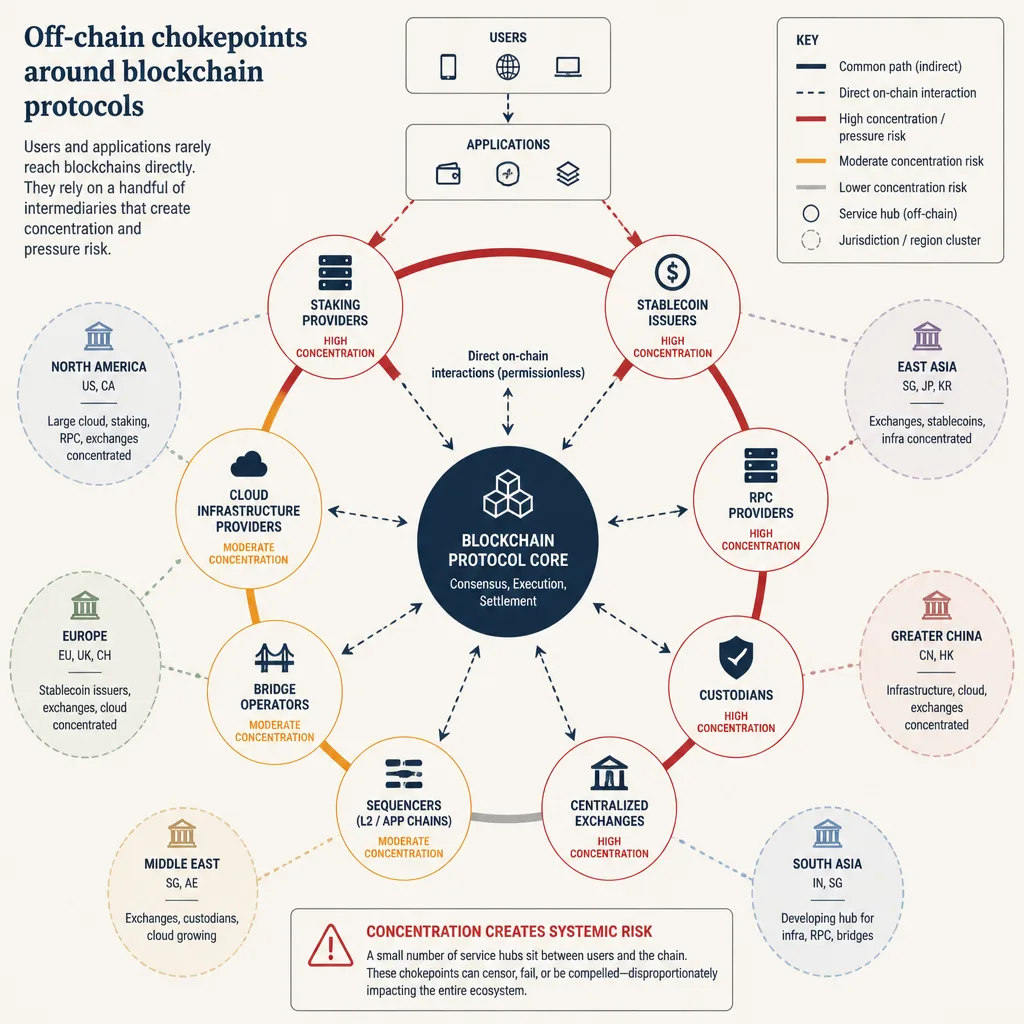

4. Regulatory choke points that centralize control off-chain

Decentralized on-chain does not mean resilient at the edges

Crypto often talks as if protocol design alone determines resilience. In reality, control often reappears at the service layer.

A chain may have broad validator distribution and still depend heavily on a few staking providers, stablecoin issuers, custodians, RPC services, wallet gateways, or centralized sequencers. Those become pressure points.

This matters especially for rollups. An L2 may inherit settlement security from Ethereum while still relying on a single sequencer, upgrade keys, and a narrow set of asset issuers or RPC providers.

Where the choke points usually are

The most common ones are:

- large staking and liquid staking providers

- stablecoin issuers such as Circle or Tether

- dominant RPC services such as Infura or Alchemy

- custodians and centralized exchanges

- sequencers and bridge operators

- cloud hosting and app distribution channels

Warning signs

Be cautious when you see:

- dependence on a handful of regulated intermediaries

- jurisdiction concentration in one or two countries

- censorable infrastructure dominating access

- wallet or RPC providers acting as practical gatekeepers

- large portions of activity mediated by regulated issuers

Regulation is not automatically fatal. Concentrated, enforceable control is the real problem.

5. Bridge contagion and externalized trust failures

A chain can fail because of infrastructure it does not control

Many ecosystems do not secure their own value end to end. They import value through bridges, wrapped assets, and canonical transfer routes. That means some of their most important trust assumptions sit outside their own consensus.

This is why bridge risk is existential, not peripheral. If the main path that brings liquidity into a chain is fragile, the chain inherits that fragility.

Bridge failures damage more than balances

The Ronin and Wormhole exploits made this clear in different ways: bridge failures do not just cause direct losses. They undermine trust in collateral, impair apps built on wrapped assets, and fragment liquidity across competing versions of what is supposed to be the same asset.[^1][^2]

Even if the base chain was not hacked, its ecosystem can still absorb a long reputational and liquidity discount. Multichain’s collapse showed another version of the problem: when a bridge or routing layer breaks, downstream ecosystems suddenly discover how dependent they were on it.[^3]

Warning signs

Watch for:

- one dominant bridge route for most value transfer

- heavy dependence on wrapped assets

- multisig-heavy controls or opaque recovery assumptions

- repeated bridge pauses or emergency interventions

- fragmented canonical liquidity across multiple wrappers

Some chains are not only secured by their consensus. They are also exposed to the weakest major bridge their users rely on.

6. Validator centralization behind the appearance of decentralization

Node count is a weak proxy

A high validator count is one of crypto’s favorite vanity metrics. It can be useful, but by itself it says very little about real control.

What matters is who can coordinate censorship, threaten liveness, influence upgrades, or dominate incident response. A thousand validators can still reduce to a handful of meaningful operators once you account for delegated staking, liquid staking, custodial concentration, or cloud dependence.

Control often concentrates through market structure

This is why liquid staking dominance deserves scrutiny. If too much stake flows through a small number of providers, the network may look distributed while becoming economically centralized.

The same logic applies in proof-of-work through mining pools. Many miners do not necessarily mean many decision-makers if block production is concentrated among a few pools.

Infrastructure concentration matters too. If a large share of validators runs on the same cloud provider or in the same region, decentralization can fail in a correlated way under stress.

Warning signs

Pay attention to:

- top operators controlling enough share to affect liveness or finality

- concentrated delegation to a few providers

- widespread dependence on the same cloud or data center stack

- high hardware requirements that deter independent operators

- upgrades that seem to require a small inner circle to coordinate

Healthy decentralization means distributed power, not just distributed labels.

7. Economic irrelevance even when the chain technically survives

The quietest failure mode is often the most common

A chain may avoid hacks, maintain uptime, and still become irrelevant because users, developers, and liquidity move elsewhere. It survives technically, but not competitively.

That decline is often gradual until it suddenly looks obvious. Grants keep dashboards busy. Airdrops create bursts of activity. TVL holds up because of mercenary capital. Then incentives fade and very little remains.

Durable demand is harder to fake

The key question is not whether there is activity. It is whether the activity is durable.

Real ecosystem strength usually shows up in signals that are harder to manufacture: developers returning release after release, apps with retention, stablecoin growth that persists, and users who stay without being paid to do so.

Warning signs

Look for:

- stagnant developer activity

- weak app quality despite generous incentives

- mercenary bridge inflows and fast outflows

- declining stablecoin base or shallow liquidity

- no clear reason users choose the chain beyond subsidies

A chain can recover from a hack. It is much harder to recover from becoming unnecessary.

A practical resilience checklist

No single metric can tell you whether a network is healthy. A better approach is to think in clusters. You are looking for reinforcing weaknesses, not isolated blemishes.

Use these seven questions:

- Security budget: Is security earned by real demand, or mostly subsidized by inflation, grants, or temporary incentives?

- Governance concentration: Who can change the rules in practice?

- Client diversity: Could one software bug impair most of the network?

- Off-chain choke points: Which actors could regulators or counterparties pressure to disrupt usage?

- Bridge dependence: What external trust assumptions support the chain’s major assets and liquidity?

- Validator power distribution: Who controls liveness, censorship resistance, and upgrade coordination in reality?

- Economic relevance: Why do users and developers stay when incentives fade?

A chain does not need to score perfectly on all seven. But weakness across several at once is where risk becomes nonlinear. Declining fees plus validator concentration plus dominant wrapped assets is far more serious than any one metric alone.

What strong networks tend to have in common

Strong networks rarely depend on one miracle metric. They have redundancy across layers.

They show real fee demand rather than inflated activity. Power is spread across validators, software clients, and governance actors. Liquidity can move through more than one trusted path. Developers stay because the ecosystem offers something durable, not because treasury incentives are temporarily generous.

Most importantly, resilient chains can absorb stress without leaning too heavily on any single subsidy, client, operator, bridge, or political gatekeeper. That is what resilience looks like in practice.

Conclusion

Most blockchains do not die in one dramatic event. They fail as systems lose security, neutrality, liquidity, legitimacy, or relevance over time.

That is why price is such a poor early warning signal. By the time the market fully reprices a chain’s fragility, the deeper problems were often already visible elsewhere: weak fee quality, concentrated control, fragile bridge assumptions, shrinking developer conviction.

The useful habit is to stop asking whether a chain is “alive” and start asking what keeps it alive. If the answer depends on one client, one operator class, one bridge, one issuer, or one subsidy, the risk is higher than the marketing suggests.

The healthiest networks are not the ones that look unstoppable in easy periods. They are the ones that can take stress without quietly becoming something their users no longer trust.

FAQ

What does it mean for a blockchain to die?

A blockchain usually dies functionally before it dies literally. It may still produce blocks, but if it loses security, credible neutrality, liquidity, developer activity, or user trust, it can be effectively dead long before any formal shutdown.

Can a blockchain be alive technically but dead economically?

Yes. A chain can remain online while losing the reasons people use it. If liquidity dries up, developers leave, apps stagnate, and demand depends mostly on subsidies, the network may survive technically while becoming economically irrelevant.

What is the biggest warning sign a blockchain is failing?

There is rarely one decisive metric. The clearest early signal is usually a cluster of weaknesses: declining real fee revenue, rising validator or governance concentration, heavy bridge dependence, and weakening ecosystem demand at the same time.

Why is token price a poor way to judge chain health?

Price is often a lagging indicator. A token can stay strong while the network underneath becomes more fragile through subsidized activity, concentrated control, weak security economics, or declining developer commitment.

How does a weak security budget threaten a blockchain?

Security has to be funded. If a chain cannot support validators or miners through durable fee demand and instead relies mostly on inflation or subsidies, the cost to attack or destabilize the network may become too low relative to the value it secures.

Why does validator count not equal decentralization?

Because many validators can still map back to a small number of operators, staking providers, cloud hosts, or pools. What matters is effective control over liveness, censorship, upgrades, and incident response, not just the raw number of nodes.

What is governance capture in crypto?

Governance capture happens when a small group of insiders, whales, foundations, delegates, or aligned operators can change important rules with limited resistance. Once users believe the system is no longer credibly neutral, trust and economic activity can leave quickly.

Why is client monoculture dangerous for blockchains?

If most validators run the same client implementation, one critical bug can become a network-wide problem. A chain may look decentralized at the validator level while remaining dangerously centralized at the software level.

How can bridge risk threaten a blockchain that was not hacked?

Many chains depend on bridged assets for liquidity, collateral, and user activity. If a major bridge fails, wrapped assets can lose trust, apps can break, and the chain may suffer a lasting liquidity and reputational shock even if its own consensus remains intact.

What should investors and developers monitor monthly?

A practical monthly dashboard includes real fee revenue, issuance dependence, validator or pool concentration, governance turnout on major proposals, client diversity, dominant bridge exposure, stablecoin concentration, and trends in developer and user retention.