Two tokenized Treasury products can hold similarly conservative assets and still work very differently in practice. One may suit a U.S. treasury team with low minimums and a familiar fund structure. Another may be limited to non-U.S. institutions, require wallet whitelisting, and depend on issuer-run liquidity rails rather than open markets.[^1][^2]

That is the main mistake to avoid in 2026. The important question is not simply which product holds T-bills. The better question is who can legally hold it, how it moves, how redemptions work, what the minimums are, and whether liquidity comes from real secondary markets or mainly from the issuer.[^1][^3][^4]

For DAO treasuries, funds, and DeFi power users, those differences are decisive. A product can look attractive on a yield dashboard and still be unusable because of your entity structure, custody setup, or redemption needs. This guide compares five of the most relevant names: BUIDL, USYC, BENJI, OUSG, and USDY.

The comparison that actually matters

Similar collateral does not mean similar usability

The easiest way to misread this market is to treat tokenized T-bills as interchangeable forms of onchain cash. They are not.

Some products function like regulated fund access with blockchain rails. Others are gated wrappers. Others are note-based instruments built for greater transferability or operational flexibility for eligible non-U.S. users, but with a different legal claim and redemption path.[^3][^5]

USYC is a good example. It is aimed at institutions outside the United States, requires onboarding and wallet whitelisting, and has a stated $100,000 minimum. Subscriptions and redemptions run through USYC Teller in USDC, including 24/7/365 flows, but that liquidity still depends on issuer infrastructure rather than a broad public market.[^1]

USDY shows a different kind of complexity. In some ways it behaves more like a token, and it is available to eligible non-U.S. individuals as well as institutions, but it is a tokenized note rather than a straightforward fund share. Depending on when it was issued, its backing can include short-term U.S. Treasuries, ETF shares, or bank demand deposits.[^3] That is not a minor legal detail. It changes the comparison.

Core thesis: access and liquidity matter more than yield

If you remember one thing, make it this: in tokenized T-bills, similar collateral does not make products interchangeable. The product you can actually hold, transfer, and redeem is the one that matters.

For most allocators, legal access comes first. Redemption mechanics come second. Transferability and secondary liquidity come third. Yield is important, but it comes after those filters.

Start with the decision, not the token

A simple decision tree is more useful than a ranking list.

If you are a U.S. individual or U.S.-centric treasury

Start with BENJI. Not because it is always the best option, but because it looks most familiar to many U.S. operators: a U.S.-registered government money fund with onchain rails.[^6] Franklin’s 2026 prospectus also makes BENJI notably accessible on some networks, with published minimums as low as $20 on Stellar and $100 on Aptos, Base, and Solana, though eligibility still depends on network and account type.[^6]

OUSG may also be relevant for some sophisticated entities, but only if they can meet Ondo’s qualified-access onboarding requirements.[^4][^7]

If you are a non-U.S. institution focused on 24/7 onchain liquidity

USYC belongs near the top of the list. It is built for institutional onboarding, whitelist-based access, and USDC subscription and redemption through issuer rails.[^1] That makes it less open, but often more predictable for treasury and collateral workflows.

If you need collateral utility in crypto trading workflows

BUIDL and USYC are the names to watch most closely.

USYC already leans into collateral-style usage through its teller model and optional Private Liquidity Teller, which Hashnote says can be configured to provide up to 100% instant USDC liquidity in special cases, with additional fees.[^1] BUIDL, meanwhile, has increasingly been positioned through Securitize as an institutional product with growing collateral relevance, but key operating details still need to be confirmed directly from official issuer and distributor materials before making a firm recommendation.[^8]

If peer-to-peer transferability matters most

Be careful. Tokenized does not mean freely transferable.

OUSG can move 24/7, but only between investors who have already onboarded to Ondo’s qualified-access funds.[^4] USYC also requires onboarding and wallet whitelisting.[^1] BENJI and BUIDL should not be assumed to function like unrestricted stablecoins. USDY may feel more transferable in practice, but it remains jurisdictionally constrained and has a different legal profile from direct fund-share products.[^3]

If you want the lowest onboarding friction

BENJI is the clearest candidate among the five, at least based on publicly available 2026 documentation. Franklin publishes concrete network minimums and supports retail-style access on Stellar, while other networks may require separate eligibility review.[^6]

That does not make BENJI the most composable product. It makes it the easiest to understand if your team wants a familiar regulated-fund path.

These products are not solving the same problem

BUIDL: institutional tokenized fund access through Securitize

BUIDL is best understood as institutional access to BlackRock-managed liquidity exposure through Securitize. Public materials clearly show that it is distributed there, but the operating details buyers care about most, including live minimums, redemption cutoffs, fees, and full chain support, are not transparent enough in open primary documentation to state confidently here without overreaching.[^8]

That matters on its own. If a treasury team cannot easily verify the mechanics, operational certainty is lower even if the brand is strong.

USYC: non-U.S. institutional collateral and cash-management rail

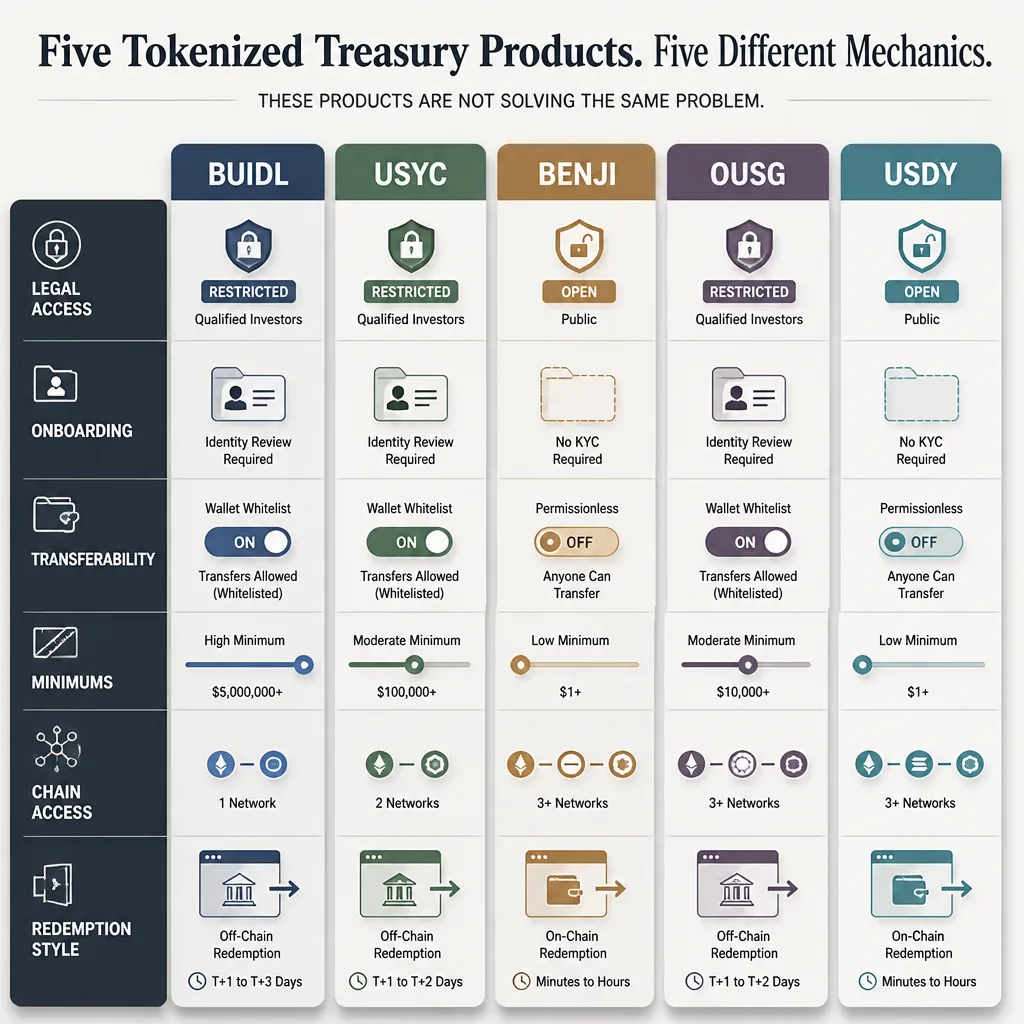

USYC is one of the most operationally explicit products in the category. It is available only to institutions outside the United States, uses onboarding plus wallet whitelisting, and has a $100,000 minimum investment.[^1] Structurally, Hashnote describes USYC as an onchain representation of fund shares recorded at the transfer-agent level.[^9]

Its liquidity story is strong, but specific. You can mint and redeem with USDC 24/7/365 through the teller. But the token price is reported once per business day, and the same-price subscription and redemption window described by Hashnote shows that 24/7 access does not mean continuous market-style price formation.[^2]

BENJI: U.S.-registered onchain money fund with retail and institutional lanes

BENJI is tied to Franklin OnChain U.S. Government Money Fund, a U.S.-registered government money market fund.[^6] That makes it the most regulation-familiar option for many U.S. users.

The operational detail that stands out in 2026 is Franklin’s published minimums by network: Stellar $20, Aptos $100, Base $100, Solana $100, Polygon $1,000, Arbitrum $1,000, Avalanche $100,000, and Ethereum $5,000,000.[^6] Those numbers show why supported chains can be a misleading comparison point unless you also ask: supported for whom, at what minimum, and through which access channel?

OUSG: tokenized Treasury exposure for qualified, onboarded users

OUSG is a gated qualified-access fund product, not a general-purpose yield token. Ondo says any investor eligible for its qualified-access funds and fully onboarded may invest, and OUSG tokens may be transferred only among already onboarded qualified-access investors.[^4][^7]

Its liquidity design is one of the most interesting in the segment. Instant minting and redemption are available 24/7/365, with a $5,000 minimum for instant transactions, but they are subject to rolling 24-hour limits shown on Ondo’s interface.[^4][^10] For larger flows, the non-instant lane remains available, with a $100,000 minimum investment, $50,000 minimum redemption, and next-business-day settlement for requests submitted before 4 p.m. ET in typical conditions.[^4][^11]

USDY: broader-access yield token with a different legal structure

USDY is not just a more accessible version of OUSG. It is a different product category.

Ondo describes USDY as a tokenized note, now under Ondo Global Markets, available to qualifying non-U.S. individual and institutional investors.[^3] It comes in two operational forms: USDY, where the reference price rises over time, and rUSDY, where the token rebases while the price stays near $1.[^3]

That distinction matters for accounting, integrations, and collateral treatment. So does the redemption path. Ondo says USD redemptions are wired to non-U.S. bank accounts, while USDC redemption can be available through Ondo Global Markets (BVI) Limited. On some networks, minting and redeeming requires contacting support and meeting a $5,000 minimum.[^3]

A six-filter framework for real-world fit

Before looking at a table, use these six filters. They usually decide the outcome faster than yield comparisons.

1. Who can legally buy and hold it?

This is the first eliminator.

- USYC: non-U.S. institutions only.[^1]

- USDY: qualifying non-U.S. individuals and institutions.[^3]

- OUSG: qualified-access investors who complete onboarding.[^4][^7]

- BENJI: depends on share class, network, and eligibility channel, but clearly includes a U.S.-registered fund pathway.[^6]

- BUIDL: institutional and Securitize-distributed; exact live access details should be checked directly.[^8]

2. Can it move wallet to wallet, or only within controlled rails?

Transferability is usually narrower than many buyers expect.

USYC and OUSG both depend on controlled onboarding and wallet permissions.[^1][^4] BENJI and BUIDL may also involve network- or channel-specific restrictions.[^6][^8] USDY is the most token-like conceptually, but it is still not legally unrestricted.[^3]

3. What are the real minimums and onboarding burdens?

Minimums vary sharply.

USYC starts at $100,000.[^1] OUSG has a $5,000 instant lane, but larger or fallback flows use non-instant minimums of $100,000 to invest and $50,000 to redeem.[^4] BENJI ranges from $20 to $5,000,000 depending on network.[^6]

4. How do fees actually show up?

Headline expense ratios do not tell the whole story.

OUSG charges a 0.15% management fee, waived through July 1, 2026, with fund expenses capped at 0.15% per year, and instant transactions may carry additional fees.[^12] USYC’s stronger-liquidity arrangements can also involve added fees.[^1] For BUIDL and BENJI, fee details should be verified against live primary documents before relying on them in an internal treasury memo.

5. Which chains are truly supported for your account type?

A chain logo is not the same as operational access.

Franklin’s BENJI network list is useful because it shows economic differences by chain directly in the prospectus.[^6] Ondo’s USDY documentation explicitly notes that some networks require manual support contact for minting and redeeming.[^3] In practice, available on chain X can still mean awkward to use on chain X.

6. How do redemptions work in normal and stressed conditions?

This is where serious buyers should spend the most time.

USYC offers 24/7 USDC redemption through the teller, with optional private liquidity arrangements for special cases.[^1] OUSG offers instant redemptions, but only within daily limits, plus a non-instant business-day route.[^4][^10][^11] USDY splits redemption between bank-wire and stablecoin paths depending on route and entity.[^3]

Side-by-side comparison

| Product | Legal/investor access | KYC/onboarding path | Transferability | Minimum | Supported chains | Redemption mechanics | Best fit |

|---|---|---|---|---|---|---|---|

| BUIDL | Institutional; verify live terms | Securitize-led onboarding | Likely permissioned; verify live rules | Not confirmed publicly enough | Expanding; verify live list | Needs direct confirmation from issuer/distributor docs | Institutions prioritizing brand and possible collateral workflows |

| USYC | Non-U.S. institutions only[^1] | Full onboarding + wallet whitelisting[^1] | Controlled/whitelisted[^1] | $100,000[^1] | Multi-chain, issuer-supported[^1] | 24/7 USDC via Teller; optional paid private liquidity[^1] | Non-U.S. treasury and collateral management |

| BENJI | U.S.-registered MMF lane; eligibility varies by network/channel[^6] | Fund/account onboarding | Not universally frictionless; network/channel dependent[^6] | $20 to $5,000,000 depending on network[^6] | Stellar, Aptos, Base, Solana, Polygon, Arbitrum, Avalanche, Ethereum[^6] | Fund redemption path; check current channel specifics | U.S.-centric treasury teams wanting regulated MMF structure |

| OUSG | Qualified-access investors only[^4][^7] | Ondo onboarding | Transferable only among onboarded investors[^4] | $5,000 instant; $100k invest / $50k redeem non-instant[^4] | Ondo-supported qualified-access rails | Instant within limits; non-instant next-business-day typical if before 4 p.m. ET[^11] | Sophisticated funds/DAOs with qualified-access eligibility |

| USDY / rUSDY | Qualifying non-U.S. individuals and institutions[^3] | Ondo Global Markets eligibility path | More token-like, but still jurisdictionally restricted[^3] | $5,000 on some support-assisted networks[^3] | Multi-network, but not always self-serve[^3] | USD wire to non-U.S. bank accounts; USDC via Ondo Global Markets route[^3] | Non-U.S. users wanting broader token utility |

What buyers often miss

Issuer redemption is not the same as market liquidity

A product can be liquid through the issuer and still have thin secondary markets.

That is not necessarily a flaw. It simply means your exit path depends on counterparty processes, cutoffs, limits, and service capacity rather than open exchange depth.[^1][^10][^11]

A supported chain is not the same as practical availability

BENJI makes this especially clear. The same product can appear on many networks while having very different minimums and eligibility requirements depending on the chain.[^6]

Direct fund exposure is different from a note-like wrapper

USYC and BENJI sit closer to direct fund-access logic.[^6][^9] USDY does not. It is a note, and the backing language itself varies by issuance date.[^3] If your policy team cares about legal claim, accounting treatment, or bankruptcy remoteness, that distinction matters.

Treasury policy may rule out the best-looking option

Many DAOs and funds find out too late that the product with the best apparent liquidity story is unusable under their entity type, signer structure, custody provider, or governance process.

Use-case guidance by buyer type

For DAOs managing stablecoin idle cash

Most DAOs should begin with a blunt legal question: can the DAO entity itself pass onboarding and hold the asset under policy? If not, the comparison stops there.

For eligible and more sophisticated DAOs, OUSG may fit if they want a qualified-access structure with clear instant and non-instant liquidity lanes.[^4] If the DAO wants broader downstream token behavior, USDY may look more attractive, but only if the non-U.S. eligibility rules and redemption path are acceptable.[^3]

For funds and prop desks seeking collateral efficiency

USYC is currently one of the most practical fits for non-U.S. institutions that want treasury parking plus USDC-based liquidity operations.[^1] BUIDL may also matter here, especially where exchange collateral acceptance or institutional counterparty recognition matters, but buyers should verify live operating terms directly before allocating.[^8]

For DeFi-native users prioritizing composability

USDY and rUSDY are usually the most relevant because they were designed with more token-like behavior in mind.[^3] But composability should not be confused with simplicity. Rebasing versus appreciating-token mechanics affect bookkeeping, collateral integrations, and smart-contract compatibility.

For teams that want the most familiar regulatory structure

BENJI is the clearest starting point. A U.S.-registered government money fund with explicit onchain distribution is easier for many finance and compliance teams to evaluate than a more novel wrapper or offshore note structure.[^6]

Buyer checklist before allocating

Legal and compliance

- Is your entity type eligible to buy, hold, and transfer the token?

- Are U.S. person restrictions, accredited-investor standards, or qualified-purchaser rules relevant?

- Can downstream recipients legally receive the token?

Operations and custody

- Does your custodian support the required chain and token standard?

- Do wallets need to be whitelisted in advance?

- Who controls redemptions: treasury ops, fund admin, or a service provider?

Liquidity and redemption

- Can you redeem into fiat, stablecoin, or both?

- Are there daily instant limits?

- What are the cutoff times for non-instant redemptions?

- What happens on weekends, month-end, or during stress events?

Counterparty and smart-contract risk

- Are you relying on issuer teller infrastructure, OTC facilitation, or actual market depth?

- Is there a private liquidity arrangement, and what does it cost?

- Which contracts, bridges, or oracles sit in the path?[^2][^10]

Governance and policy for DAOs and funds

- Does the investment policy permit direct fund shares, notes, or only cash equivalents?

- Is a rebasing token operationally acceptable?

- Can the team explain the redemption path in one page to auditors, directors, or governance voters?

Conclusion

The right tokenized T-bill product in 2026 is not the one with the most attention. It is the one your treasury can legally hold, operationally support, and reliably redeem when it matters.

That usually narrows the field quickly. BENJI is the most familiar route for many U.S.-centric users.[^6] USYC stands out for non-U.S. institutional treasury and collateral workflows.[^1] OUSG is compelling for qualified-access investors who want issuer-managed instant liquidity, as long as they understand the limits.[^4][^10] USDY is useful when broader non-U.S. token utility matters more than direct fund-share purity.[^3] BUIDL remains important, but serious buyers should confirm its current mechanics directly before treating it as interchangeable with the others.[^8]

In this market, access and redemption are not side details. They are the product.