Stablecoins Explained: How USDT, USDC, and DAI Work, Where the Real Risks Are, and How to Use Them Safely

Stablecoins are often called “digital dollars,” but that label misses the point: each one comes with a different set of risks.

That is why two tokens can both trade near $1 and still behave very differently under stress. One may be backed by reserves held by a company. Another may depend on overcollateralized crypto in smart contracts. A third may lean mostly on market incentives and confidence. They aim for the same result, but they do not get there the same way.

This guide starts with a simple question: what keeps USDT, USDC, DAI, and similar assets near $1? Then it moves to the practical questions that matter more in real use: what causes depegs, which risks matter most, and how do you avoid mistakes when sending, holding, or parking money in stablecoins?

If you remember one thing, make it this: a stablecoin is a tool for moving and holding cash-like value onchain, not risk-free cash.

What stablecoins are and why people use them

A simple mental model

A stablecoin is an onchain token designed to track a reference asset, usually the US dollar. In practice, that means it is supposed to stay close to $1.

The most useful way to think about a stablecoin is not as digital cash, but as an onchain IOU with a target price. That framing leads to better questions: who issued it, what backs it, who can redeem it, and what could break?

For example, if you hold USDC in a wallet, you do not hold a bank deposit. You hold a token issued under a specific system with its own reserves, redemption rules, and controls. It may work like dollars in many crypto use cases, but it is not the same as dollars in a bank account.

Why people use them instead of volatile crypto

Stablecoins solve a practical problem. Bitcoin and Ether can move several percent in a day. That volatility may suit speculation, but it is less useful for pricing goods, moving exchange balances, or sending payments where the receiver expects the same value on arrival.

A trader might use USDT to move between exchanges without touching the banking system. A freelancer might prefer USDC on a low-fee chain for cross-border payments. A DeFi user may hold DAI to stay onchain without direct BTC or ETH price exposure.

In each case, the goal is usually not growth. It is stability, transferability, and onchain convenience.

Why “stable” does not mean safe

“Stable” refers to the price target, not the absence of risk.

A stablecoin can trade near $1 for years and still carry meaningful tail risk. Reserves may be questioned. Banking access may be disrupted. A bridge may fail. An exchange or app holding your tokens may freeze withdrawals. The token can look stable right up until one of those hidden layers matters.

That is why understanding the risks matters more than memorizing ticker symbols.

How the main types of stablecoins work

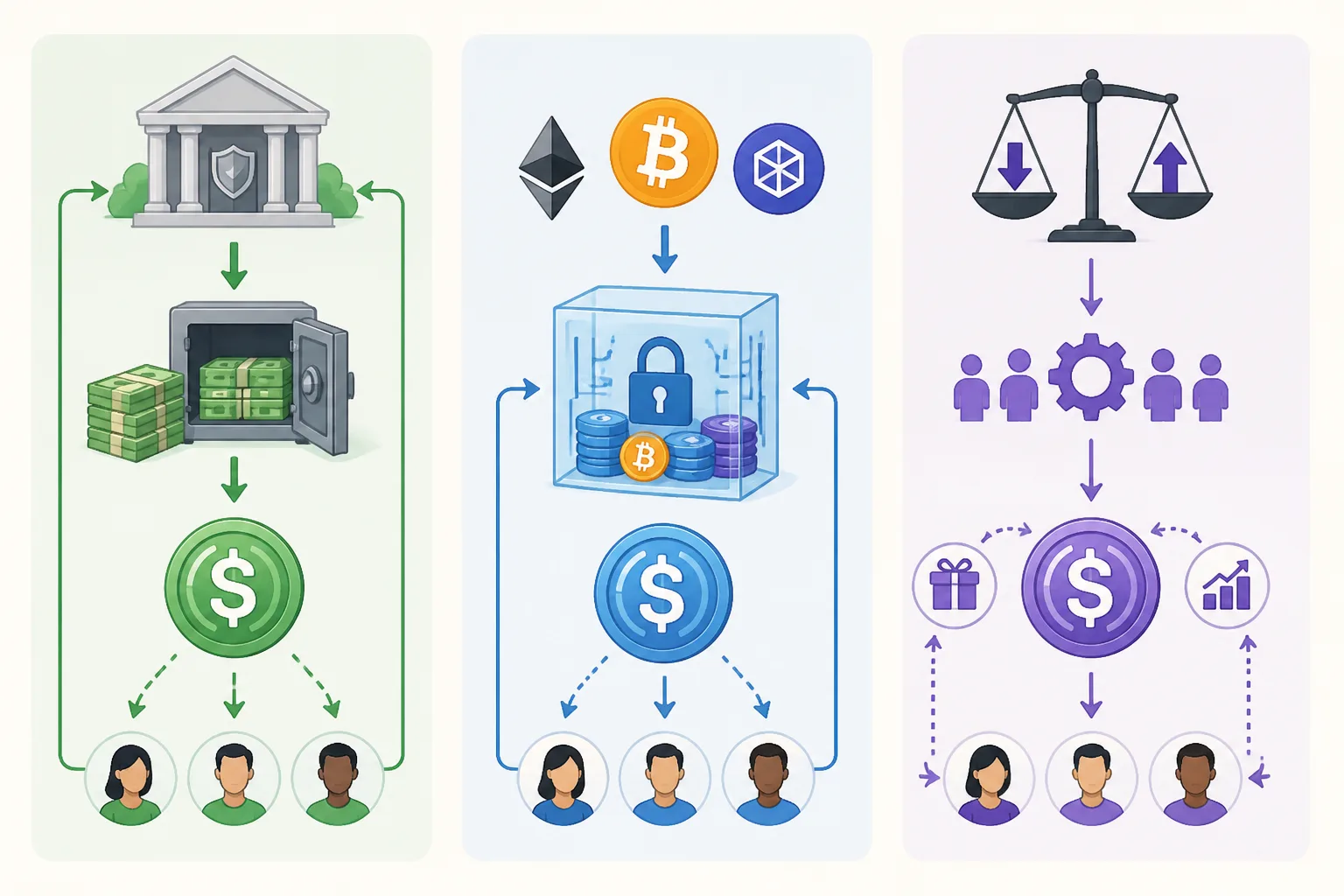

Fiat-backed stablecoins: USDT and USDC

Fiat-backed stablecoins are issued by a company that says each token is backed by reserve assets such as cash, Treasury bills, and other short-duration instruments.[^1][^2]

USDT, issued by Tether, and USDC, issued by Circle, are the main examples. The model is straightforward: approved participants deliver dollars or equivalent assets to the issuer and receive newly minted tokens. In some cases, they can also redeem tokens back through the issuer’s process.[^1][^2]

Why does this help maintain the peg? Because if the token moves too far from $1, arbitrageurs have an incentive to trade against that gap and push the price back toward parity.

Where can this model fail? Mostly at the trust layer. If the market stops believing the reserves are real, liquid, or accessible, the peg can weaken before anything formally breaks.

Crypto-backed stablecoins: DAI

Crypto-backed stablecoins such as DAI take a different approach. Instead of relying mainly on offchain reserves, users lock collateral into smart contracts and mint stablecoins against it, usually at a ratio above 100%.

For example, someone might lock $150 worth of collateral to mint $100 worth of DAI. If the collateral falls too much, the position can be liquidated to protect the system.

Why does this support the peg? Because the token is backed by excess collateral, and the protocol uses liquidation rules, incentives, and governance settings to stay solvent.

Where can it struggle? In fast market crashes, oracle failures, weak liquidation conditions, or when collateral becomes too correlated with the broader crypto market. It is also worth noting that DAI’s backing has changed over time and can include indirect exposure to centralized assets. “Decentralized” does not mean free of centralized dependencies.

Algorithmic stablecoins

Algorithmic stablecoins usually try to maintain a peg through supply adjustments, secondary tokens, or incentive mechanisms instead of hard reserve backing.

The idea can look elegant in calm markets. If price rises above $1, increase supply. If it falls below $1, create incentives to reduce supply.

The weakness is that many of these systems depend heavily on confidence. If demand drops and the supporting token also loses value, the mechanism can turn reflexive. Instead of restoring the peg, it can accelerate the collapse.

TerraUSD (UST) is the clearest warning. Its mint-burn relationship with LUNA worked while confidence held, then unraveled in a self-reinforcing spiral once confidence disappeared.[^3] The lesson is simple: if stabilization depends more on belief than on durable backing, failure can happen quickly.

How USDT and USDC stay near $1

Issuance and redemption

At a high level, USDT and USDC stay near $1 because there is a creation and redemption loop behind them. When market participants can create tokens around $1 and redeem them around $1, the token has an anchor.

For retail users, this is often less direct than beginner guides suggest. Most people do not redeem with the issuer themselves. They use exchanges, brokers, and secondary markets. Even so, redemption access for approved participants still matters because it supports confidence across the market.

Why arbitrage matters

Arbitrage connects the target price to the market price.

If a stablecoin trades above $1, a participant who can mint or source tokens near $1 can sell them at the higher market price, increasing supply and pushing the price down.

If it trades below $1, a participant can buy discounted tokens and redeem them closer to $1, reducing supply and pushing the price back up.

That mechanism works because profit-seeking traders help enforce the peg when they trust the system underneath it.

Why the price can still move

Even strong fiat-backed stablecoins can trade above or below $1 for short periods.

That can happen during exchange-specific liquidity stress, banking disruptions, chain congestion, or broader market panic. USDC’s March 2023 depeg during the Silicon Valley Bank crisis is a good example. The market reacted to uncertainty around reserve access, and USDC fell below $1 before recovering as confidence returned.[^4]

The key distinction is between a temporary depeg and a structural break. A temporary depeg means market plumbing or confidence is under stress, but the backing and redemption logic still appear credible. A structural break means the mechanism itself is no longer trusted.

Where the real risks are: a practical framework

A useful way to evaluate any stablecoin is through five layers: reserve risk, issuer risk, depeg risk, chain or bridge risk, and platform risk.

Reserve risk

The first question is not just whether a stablecoin is backed. It is what the backing consists of, and whether those assets can be turned into cash quickly under stress.

Cash and short-dated Treasury bills are very different from long-duration or opaque assets. Frequent disclosures are better than vague claims. Third-party attestations help, even if they are not the same as a full audit.[^1][^2]

This tends to matter most during market stress. Weak reserve quality often stays hidden in calm conditions.

Issuer risk

With centralized stablecoins, you also depend on the issuer and its operating environment.

That includes the company, its banking partners, legal obligations, sanctions compliance, and business continuity. It can also include administrative controls. On some networks, major issuers can freeze or blacklist addresses in response to legal or compliance actions.

For some users, that tradeoff is acceptable because liquidity and convenience matter most. For others, especially those who value censorship resistance, it is a major concern.

Depeg risk

A depeg can come from several sources:

- Reserve concerns

- Banking interruptions

- Liquidity shocks

- Exchange-specific imbalances

- Chain-specific issues

- Structural design weakness

A dip to $0.99 is not the same as a collapse to $0.60. The practical question is whether the market still trusts the reserves, redemption path, and system design.

Chain and bridge risk

This is one of the most important and most overlooked risks.

The ticker symbol is not enough. USDC on Ethereum is not the same asset path as USDC on Solana, Tron, Arbitrum, or a third-party bridge wrapper. A native stablecoin is issued directly on that chain by the official issuer or protocol. A bridged stablecoin is a representation created through a bridge or wrapper.

Why does that matter? Because a bridge adds another failure point. If the bridge is exploited, the wrapped token can fail even if the original stablecoin remains sound.

A common mistake looks like this: someone withdraws “USDC” from an exchange to a chain the recipient does not support, or receives a bridged version that a DeFi app will not accept. The wallet may show a balance, but that does not mean the asset is usable where intended. Recovery can be difficult, expensive, or impossible.

Platform risk

Holding stablecoins on an exchange is not the same as holding them in self-custody. Depositing them into a yield app is not the same as simply keeping them in a wallet.

Once stablecoins sit inside a platform, you take platform risk too. That may include exchange insolvency, withdrawal restrictions, smart contract failure, liquidation risk, or strategy risk.

For example, if you deposit USDC into a lending app advertising 8% yield, you no longer only hold USDC risk. You also take on borrower risk, protocol risk, collateral management risk, and smart contract risk. The yield comes from somewhere, and that somewhere is additional risk.

Why some stablecoins fail and others recover

Temporary stress

USDC’s 2023 banking-stress episode is a good example of a temporary depeg. The market became concerned about reserve access after Circle disclosed exposure linked to Silicon Valley Bank, and USDC traded below $1 before recovering.[^4]

The lesson is not that reserve-backed stablecoins are perfectly safe. It is that even relatively strong systems can wobble when confidence in reserve access is shaken.

Structural failure

UST is the opposite case. Its collapse was not just a liquidity scare. The stabilization design itself broke because the system relied on reflexive confidence in LUNA and incentives that stopped absorbing sell pressure.[^3]

That is what structural failure looks like: the mechanism no longer restores trust because the mechanism itself is what the market no longer trusts.

The takeaway from algorithmic collapses

The practical lesson is simple. When a stablecoin depends mostly on confidence rather than credible backing, confidence is not a side issue. It is the core support.

And confidence can vanish faster than code can respond.

How to use stablecoins safely

For payments

For payments, the biggest risk is often operational, not financial.

Before sending, confirm the exact token, the exact chain, and whether the recipient supports that combination. USDC on Ethereum and USDC on Solana are different routes. Lower fees on one chain do not help if the recipient only accepts another.

A good workflow is simple: verify the contract from an official source, confirm recipient support, and send a small test transaction if this is a new setup.

For trading

For trading, liquidity usually matters most.

That is why many traders prefer USDT. It tends to have deeper liquidity and broader exchange support. If your main goal is moving collateral quickly between venues, depth and acceptance may matter more than other factors.

USDC is also widely used, but the right choice depends on where you trade, which pairs you need, and which risks matter most to you.

For savings or idle cash

If your goal is to hold cash-like value onchain, start with preservation, not yield.

A plain stablecoin still carries issuer and chain risk. Adding yield adds another layer, usually through lending, leverage demand, market-making, or protocol incentives. Higher yield usually means more hidden complexity.

For larger balances, some users reduce concentration risk by splitting funds across more than one issuer or custody setup. That does not remove risk, but it can reduce single points of failure.

Stablecoin safety checklist

Before you use a stablecoin, verify these five things:

- Confirm the exact token and chain. Do not rely on the ticker alone.

- Verify the official contract address. Use issuer or protocol documentation.

- Prefer large, liquid, native versions over obscure bridged assets.

- Check issuer transparency and redemption history. Review current reserve disclosures and market reputation.[^1][^2]

- Avoid concentrating all exposure in one issuer or one platform.

One more rule helps beginners: self-custody removes exchange counterparty risk, but it does not remove issuer risk, bridge risk, or user error. It helps in some ways, not all.

USDT vs USDC vs DAI: which fits which use case?

Best fit for trading liquidity

USDT is often the strongest fit for trading-focused users because of its deep liquidity and broad exchange support.

If your priority is moving in and out of positions quickly, that may matter more than almost anything else.

Best fit for transparency-focused users

USDC is often a better fit for users who care more about reserve reporting, institutional-style disclosures, and a clearer trust model.[^2]

That does not make it risk-free. It just means the structure may feel more legible to users who prioritize transparency.

Best fit for DeFi-native users

DAI can make sense for users who want a more DeFi-native option and are comfortable with smart contracts, collateral composition, governance, and liquidation mechanics.

But DAI is not simple stable money. It has its own complexity, and that complexity matters before you treat it as a default savings asset.

The better question to ask

There is no universal winner.

The more useful question is: what job are you trying to do?

- If you need trading liquidity, USDT may be the practical choice.

- If you value disclosures and institutional framing, USDC may fit better.

- If you prefer DeFi-native design and understand protocol risk, DAI may make sense.

The right answer depends on your goal, your chain, and your tolerance for centralization, smart contract complexity, and stress behavior.

Final takeaway

Stablecoins are useful because they let people move, hold, and use dollar-like value onchain without taking full crypto market volatility.

But they are not interchangeable digital cash. Every stablecoin combines a backing model, an issuer or protocol structure, a chain path, and its own failure modes.

A simple decision framework can help you avoid most preventable mistakes:

- Backing: What supports the token?

- Access: Who can redeem it, control it, or freeze it?

- Path: Which exact chain and token version are you using?

If you apply those three checks before holding, sending, or chasing yield, you will understand stablecoins better than most users who only look at the $1 price.

FAQ

What are stablecoins in simple terms?

Stablecoins are onchain tokens designed to track a reference asset, usually the US dollar. The simplest way to think about them is as digital IOUs with a target price, not the same thing as cash in a bank account.

How do stablecoins keep their price near $1?

Different stablecoins use different mechanisms. Fiat-backed stablecoins like USDT and USDC rely on reserves and redemption, while crypto-backed stablecoins use overcollateralization and liquidation systems. In both cases, arbitrage helps push the market price back toward $1 when confidence in the mechanism holds.

What is the difference between USDT and USDC?

Both are fiat-backed stablecoins, but users often choose them for different reasons. USDT is widely used for trading liquidity across exchanges, while USDC is often preferred by users who want clearer reserve disclosures and a more institutional trust model.

Why can USDT or USDC trade below $1 if they are supposed to be stable?

A stablecoin can dip below $1 during market stress, banking disruptions, exchange-specific liquidity issues, or short-term redemption concerns. A temporary depeg does not always mean the stablecoin has failed, but it does show that confidence and market structure matter.

What causes a stablecoin depeg?

Common causes include reserve concerns, issuer or banking problems, liquidity shocks, chain-specific disruptions, bridge failures, or weak design. Some depegs are temporary. Others become permanent when the stabilization mechanism itself breaks.

How does DAI maintain its peg?

DAI is generally maintained through overcollateralized positions, liquidation rules, and protocol incentives. Users lock collateral worth more than the DAI they mint, and the system tries to keep the token near $1 through market and governance mechanisms.

Why are algorithmic stablecoins riskier?

Algorithmic stablecoins usually depend more on market incentives and confidence than on hard reserve backing. That can work in normal conditions, but if confidence breaks, the system can become reflexive and fail very quickly.

What is the difference between native and bridged stablecoins?

A native stablecoin is issued directly on a blockchain by the issuer or official system. A bridged stablecoin is a representation created through a bridge or wrapper, which adds another layer of contract, custody, or validator risk.

Are bridged stablecoins riskier than native versions?

Usually, yes. With a bridged stablecoin, you still have the base stablecoin risk, but you also add bridge risk. If the bridge fails, is hacked, or loses backing integrity, the wrapped version can break even if the original stablecoin remains sound.

Is self-custody safer than keeping stablecoins on an exchange?

Self-custody removes exchange counterparty risk, but it does not remove issuer risk, chain risk, or user error. It can improve safety in some situations, but it is not a complete solution by itself.

Does earning yield on stablecoins make them riskier?

Yes. Stablecoin yield usually comes from lending, leverage demand, market-making, or protocol incentives. That means you take extra counterparty, smart contract, or strategy risk beyond simply holding the stablecoin.

What should I verify before sending or holding a stablecoin?

Check the exact token, exact chain, official contract address, issuer credibility, and whether the recipient supports that version. It is also smart to avoid obscure bridged assets, use a test transfer when needed, and avoid concentrating all funds in one issuer or platform.