A lot of MEV commentary still reflects an older version of Ethereum: bots watch the public mempool, spot a large swap, and sandwich it before the block lands. That picture is still real. It just is no longer sufficient.

In 2026, a better definition is simpler and broader: MEV is the value that comes from controlling transaction ordering, inclusion, or information around block production.[^1] Once you look at it that way, the story expands beyond mempool bots. It includes searchers, builders, relays, validators, wallet routing, and private orderflow providers.

That is also why the usual slogans fall apart under inspection. PBS did not “solve MEV.” Private RPCs are not automatically safer. And a drop in visible sandwich attacks does not necessarily mean markets became fairer. The harder question is who gained protection, who gained power, and what became harder to see.

MEV in 2026 Is Not Just a Mempool Bot Story

Why the old explanation is no longer enough

Most retail explanations of MEV start with a DEX trade.

A user submits a large swap to the public mempool with wide slippage. A bot sees it, buys first, sells after, and captures the price move. The user gets a worse fill. That example still matters because it shows the core issue: leaked intent can be exploited.

But it no longer explains where most of the power sits.

After the Merge, Ethereum split consensus from execution. Validators propose blocks, but many do not build the most profitable block themselves. Specialized actors do that instead, and much of modern MEV now runs through a structured supply chain rather than a visible scramble among public bots.[^2][^3]

The core idea: control over ordering, inclusion, and information

That framing matters because it covers far more than sandwiching.

It includes arbitrage and backruns, which can help markets reprice. It includes liquidations, where speed and sequencing are critical. It also includes private transaction channels, where the edge is often not “attack the user in public,” but “see the order first and decide where it goes.”

MEV is not just a bot problem. It is a market structure problem.

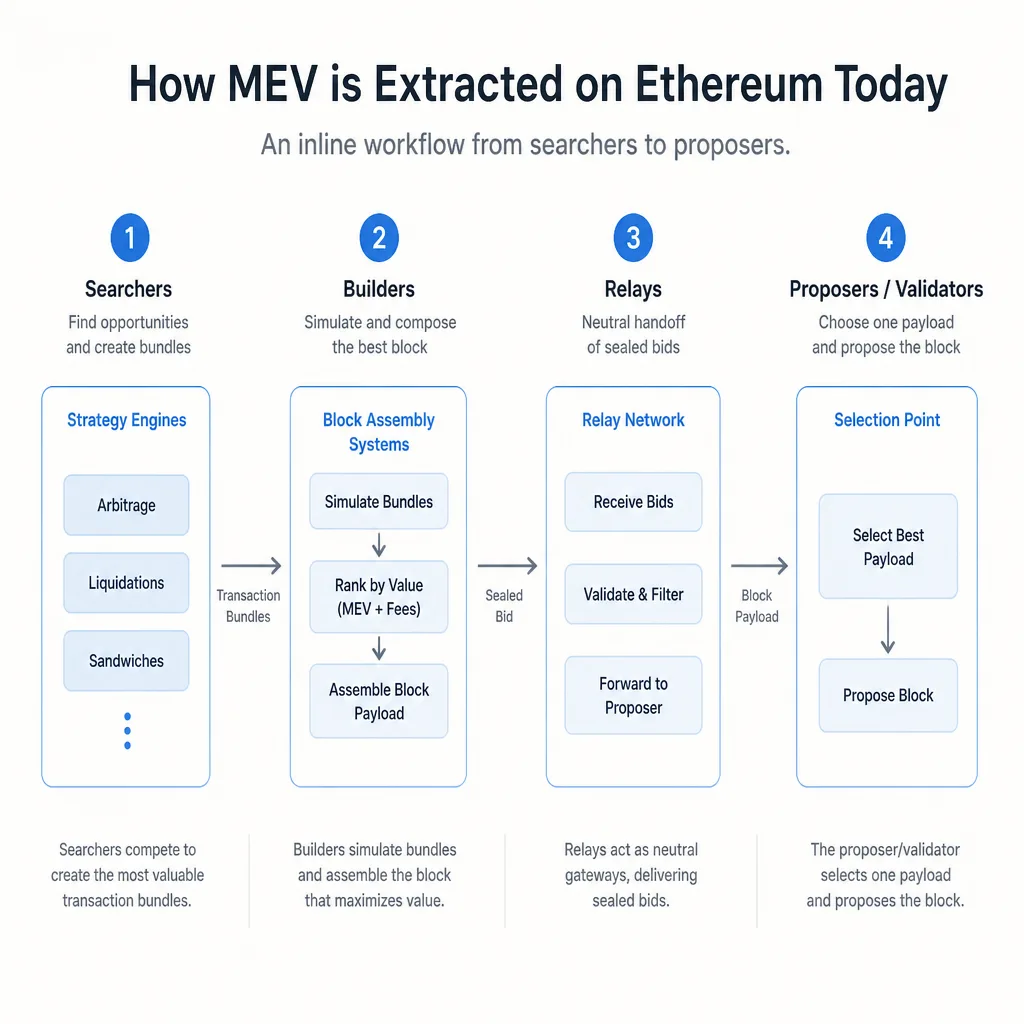

How MEV Is Extracted Today

Searchers: finding opportunities

Searchers are the strategy layer.

They look for arbitrage across DEXs, liquidation opportunities in lending protocols, backruns after large trades, and sometimes sandwich opportunities. Their edge comes from data speed, simulation, capital, routing logic, and increasingly access to orderflow.

A strong searcher is not simply watching the mempool. They are modeling state changes and packaging transactions or bundles a builder can place into a block.

Builders: assembling the most profitable block

Builders are the assembly layer.

They collect transactions and bundles, simulate different block layouts, and try to produce the most profitable valid block.[^3] That is very different from just sorting transactions by gas price. A builder is optimizing a block-level auction: what to include, in what order, with which bundles, and with what payout to the proposer.

That work is specialized for a reason. Competitive block building is infrastructure-heavy, latency-sensitive, and operationally demanding.

Relays: coordinating bids and delivery

Relays sit in the middle of the dominant out-of-protocol PBS workflow, often via mev-boost. They receive sealed bids from builders, verify basic validity conditions, and deliver the best payload to proposers.[^3][^4]

They solve a trust problem. Proposers want confidence that a promised payment is real. Builders want to avoid revealing a valuable block before selection. Relays make that exchange possible.

They also create chokepoints. That is the tradeoff.

Proposers and validators: choosing the winning block

Proposers, usually validators running PBS-compatible infrastructure, choose from the bids they can access. Their incentive is simple: pick the highest-value valid payload available.[^2][^4]

That helps explain why MEV never disappeared. It was not removed. It was routed toward specialists.

What PBS Is Actually Trying to Fix

Why block building became too specialized

Without separation, the validators best positioned to capture MEV would be those with the best internal block-building stack.

That creates an unhealthy dynamic. As block construction becomes more profitable, validators face more pressure to vertically integrate search, simulation, and networking. Over time, that favors larger operators and pushes the validator layer toward centralization.

PBS exists because “every proposer should also be an elite builder” is not a realistic equilibrium.[^5]

How PBS changes the system

PBS separates the right to propose a block from the task of building it.

In live Ethereum, that mostly happens through out-of-protocol PBS, especially mev-boost-style workflows, rather than fully enshrined PBS in the base protocol.[^3][^5] The practical result is that proposers can outsource block construction to a competitive builder market and choose among bids.

That lowers complexity for validators and shifts competition toward specialized builders.

What PBS genuinely improves

PBS deserves a fair reading.

It can improve block-building efficiency because specialists are better at aggregating bundles and optimizing payloads. It can support builder competition because multiple firms can compete for proposer selection. And it can reduce the pressure on validators to run their own sophisticated MEV infrastructure just to stay competitive.[^5]

Those are real improvements.

But they are improvements in system design and validator economics. They are not the same as fairness for users.

Why PBS Does Not Solve Fairness

Efficiency and fairness are different things

A market can become better at extracting value without becoming fairer.

That is the source of a lot of confusion around MEV. PBS can improve auction efficiency and reduce validator burden. By itself, it does not determine whether users receive neutral treatment, equal access, or transparent execution.

A cleaner machine is still a machine.

The deeper problems remain

The underlying issue is still the same: actors with better information and more control over orderflow can capture value before the market broadly sees what happened.

Searchers still compete on speed and modeling. Builders still control final block composition. Relays still mediate access. Wallets and RPC providers increasingly influence whether a transaction is public at all. None of that disappears just because proposers stopped building blocks themselves.

The asymmetry was reorganized, not removed.

Why fewer visible sandwiches can mislead

Suppose public-mempool sandwiching declines.

That might mean users are better protected. It might also mean more orderflow moved into private channels where extraction is harder to observe. Or it could mean powerful intermediaries internalized the value in ways that no longer show up as obvious public attacks.

So “fewer sandwiches” is a useful signal. It is not a full conclusion.

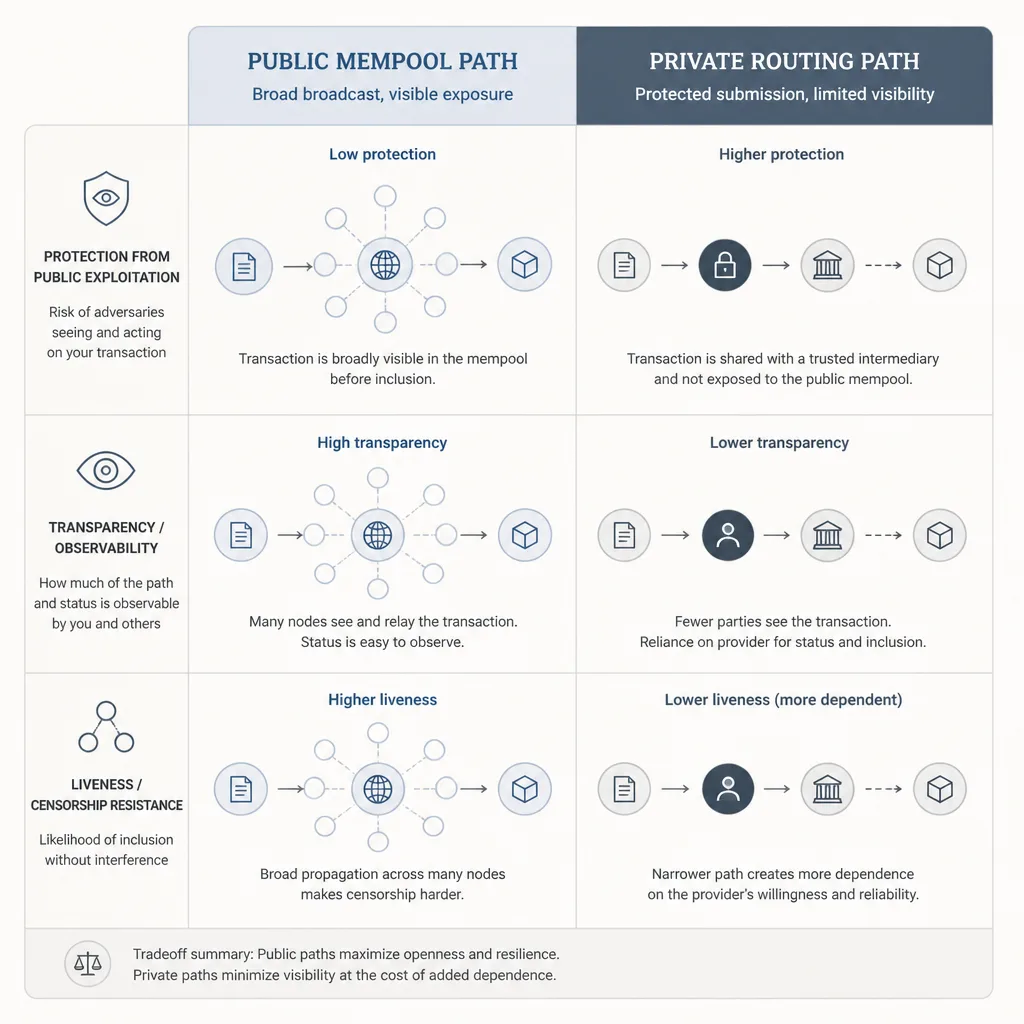

Private Orderflow: Protection for Users, Leverage for Intermediaries

Why people route transactions privately

Private orderflow means sending a transaction through a private channel instead of broadcasting it to the public mempool first.

That can happen through protected RPC endpoints, wallet routing systems, app-specific infrastructure, or execution systems that selectively forward orderflow to builders or solvers. The reason is straightforward: public visibility leaks intent.

If your trade is large, your liquidation is urgent, or your position change is market-sensitive, showing it to everyone before inclusion can be expensive.

What private routing can reduce

Private routing can be genuinely useful.

A large swap on thin liquidity is the obvious example. In the public mempool, searchers may detect it and sandwich it. Through a protected route, that same transaction may avoid visible predation and land with better execution.

Another example is a sensitive DeFi liquidation or leverage reduction during volatility. Public submission can invite copy trading, failed execution, or adverse price movement before inclusion. Private routing can reduce some of that exposure.

These are real advantages, and they help explain why wallets and users keep adopting protected transaction paths.

What private routing can increase

The cost is that one risk surface gets replaced by another.

In the public mempool, harmful behavior is at least easier to observe. In a private channel, you often cannot verify whether your transaction was selectively shared, delayed, internalized, or exposed to privileged counterparties. You may avoid a public sandwich while still having little visibility into execution quality.

Private routing also increases dependence on intermediaries. If a few wallets, RPC providers, builders, or relays control a large share of orderflow, they gain leverage over inclusion, routing, disclosure, and policy. That creates concentration risk and, in some cases, censorship risk.

Confidentiality before inclusion is not the same as neutrality after submission.

When a Private RPC Makes Sense

Good use cases

Private routing usually makes the most sense when leaked intent is costly.

That includes:

- large swaps, especially on thin liquidity

- liquidations or leverage adjustments

- arbitrage-sensitive or copy-tradeable actions

- periods of heavy volatility where failed public transactions are expensive

In those cases, protecting the transaction before inclusion may matter more than preserving maximum observability.

When the public mempool is fine

Not every transaction needs protection.

If you are making a simple transfer, a small swap, or a routine interaction where information leakage is not economically meaningful, the public mempool may be perfectly acceptable. Some users also prefer the openness of public broadcast even when it carries some exposure.

That is a valid choice. Openness has value too.

A simple tradeoff model

The cleanest way to think about the choice is as a three-way tradeoff:

| Priority | Public mempool | Private routing |

|---|---|---|

| Protection from public exploitation | Weaker | Often stronger |

| Transparency and observability | Stronger | Weaker |

| Liveness / censorship resistance | Often broader by default | Depends heavily on provider path |

No option wins on every axis.

If leaked intent is expensive, private routing may be worth it. If you care more about openness, broad propagation, or minimizing intermediary trust, public submission may be the better fit.

The mistake is looking for a universal answer.

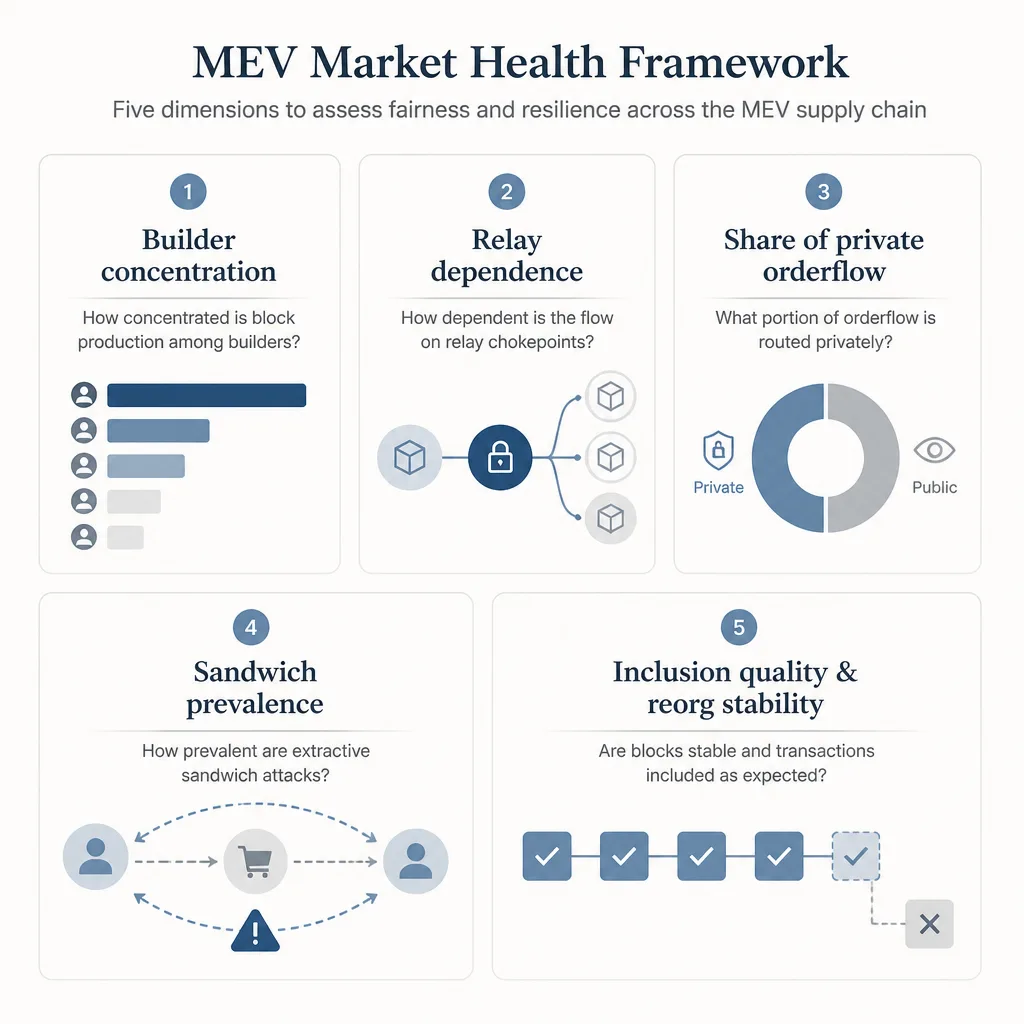

What Actually Signals a Healthier MEV Market

Builder concentration

If a small number of builders consistently win most blocks, ordering power is concentrating. That matters even if users see fewer public attacks, because concentrated builders can shape access and execution quality.

Relay dependence and censorship surface

Relays are not part of Ethereum’s base protocol in the same way validators are, but they matter in practice. If proposers depend on a narrow relay set, or dominant relays apply filtering policies, the path to inclusion becomes less open.[^4]

That is not just a plumbing detail. It is a market-health issue.

Share of private versus public orderflow

A rising share of private orderflow can mean users are protecting themselves. It can also mean more of the market is becoming opaque and dependent on a small set of intake points.

Both interpretations can be true at once.

Sandwich prevalence, reorg stability, and inclusion quality

Visible sandwich frequency still matters. So do inclusion delays, failed transaction patterns, and block stability measures such as reorg sensitivity. But each metric captures only one part of the picture.

A market can improve on one dimension while getting worse on another.

Why fairness is not one metric

Fairness is not a single number.

It is some combination of competition, openness, execution quality, censorship resistance, and how much invisible privilege exists in the routing chain. If someone says MEV has been “fixed” because one headline metric improved, that is usually a reason to look more closely.

The Honest Conclusion

PBS helped. It reduced validator-side complexity, supported specialized block building, and made the system more modular.[^5] Those are meaningful improvements.

But modular is not the same as fair.

The unresolved problem is still about power over ordering and information. Private orderflow can protect users from real harms, especially in high-value or information-sensitive transactions. It can also make the market more opaque and more dependent on a narrower set of intermediaries.

So the practical takeaway is not “always use private RPC” or “never trust private orderflow.” It is simpler than that, and less comforting: use private routing selectively when leaked intent is expensive, understand the trust assumptions you are accepting, and judge market-health claims by concentration and inclusion quality, not slogans.

A healthier MEV market would not merely hide extraction more effectively. It would spread ordering power more broadly, reduce chokepoints, and make user protection less dependent on trusting a few gatekeepers.

FAQ

What is MEV in 2026, in plain English?

MEV is the value captured by controlling transaction ordering, inclusion, or information around block production. In 2026, that extends beyond visible mempool bots to builders, relays, private orderflow providers, and wallet routing systems.

What does proposer-builder separation (PBS) do?

PBS separates block proposing from block building. Instead of every validator needing to build the most profitable block themselves, specialized builders compete to construct blocks and proposers choose among bids. That can reduce validator complexity and improve efficiency, but it does not automatically make execution fairer for users.

Did PBS solve MEV?

No. PBS changed where and how MEV is extracted, and it reduced some pressure on validators to become specialized block builders. But the deeper issue, who controls ordering, information, and access to orderflow, remains unresolved.

Why is the old mempool-bot explanation incomplete?

It still explains part of the problem, especially for public swaps vulnerable to sandwiching. But much of today’s MEV activity sits in a broader chain involving searchers, builders, relays, proposers, and private transaction routing.

What is private orderflow?

Private orderflow means sending transactions through a private channel instead of broadcasting them to the public mempool first. That can happen through private RPCs, wallet routing systems, protected transaction endpoints, or app-specific execution channels.

Are private RPCs safer?

Sometimes, but only against certain risks. A private RPC can reduce exposure to public mempool sandwiching, copy trading, or failed execution during volatility. It can also increase dependence on intermediaries, reduce transparency, and introduce censorship or inclusion risks.

When should I use a private RPC?

Private routing makes the most sense when information leakage is expensive, such as with large swaps, thin liquidity, liquidations, leverage adjustments, or volatile markets. For small transfers or routine interactions, the public mempool may be acceptable if you prefer openness and broader observability.

What are the tradeoffs of private orderflow?

The main tradeoff is protection versus transparency and liveness. You may get less public exposure and better protection from visible predation, but you also trust a smaller set of providers to handle your transaction fairly, include it promptly, and avoid censorship or opaque internalization.

Why does private orderflow raise centralization concerns?

Because routing power can accumulate in a few wallets, RPC providers, builders, or relays. Even if users see fewer visible attacks, the system may become more dependent on a small group of intermediaries that control access, inclusion, and information.

What signals a healthier MEV market?

Useful signals include builder concentration, relay dependence, the share of private versus public orderflow, censorship indicators, inclusion quality, and visible sandwich prevalence. No single metric captures fairness, so the market has to be judged through a mix of competition, openness, and execution quality.