Crypto Regulation Isn’t Just “Good” or “Bad”: A Builder’s Map of the New Compliance Stack

Most crypto regulation gets discussed as politics. Is it innovation-friendly? Hostile? Necessary? Those debates matter, but they are not where builders usually feel the pressure.

They feel it in product flows. In onboarding screens. In blocked wallets. In support tickets from legitimate users who got flagged. In bank partners asking uncomfortable questions. In the awkward moment when a risk API returns an alert and nobody has decided what happens next.

That is the real shift. Compliance is no longer just a legal topic. It is a product architecture problem.

The useful question is not whether regulation is good or bad. It is narrower and harder: what is the lightest compliance stack that credibly fits your product, counterparties, and jurisdictions without turning the UX into a maze?

Regulation is becoming a product architecture problem

Why “good or bad” is the wrong framing

For builders, regulation is rarely one thing. It is a stack of controls, policies, counterparties, and operational choices sitting between your product and the outside world.

A custodial exchange connected to fiat rails has a very different risk surface from a non-custodial DeFi front-end. A retail wallet serving users globally faces different tradeoffs from an OTC desk serving institutions. Treating them as if they need the same answer leads to bad design.

That is why the good-versus-bad framing breaks down. It is too abstract. The more useful distinction is proportionate versus mismatched.

What regulation looks like in practice

In real products, regulation usually appears as implementation requirements:

- Do you need identity checks?

- Do you need to screen wallets before deposits or withdrawals?

- Do you need to exchange sender and recipient data with another regulated provider?

- Do you need a review queue for flagged transactions?

- Do you need to block certain jurisdictions at the interface level?

These are not variations of one problem. They are separate problems that often get bundled together.

The core idea

Most serious crypto teams do not need exchange-grade compliance everywhere. But almost none should rely on vibes.

The right model is modular. Each layer answers a different question. The goal is not maximum compliance theater. It is to match controls to the actual risk your product creates.

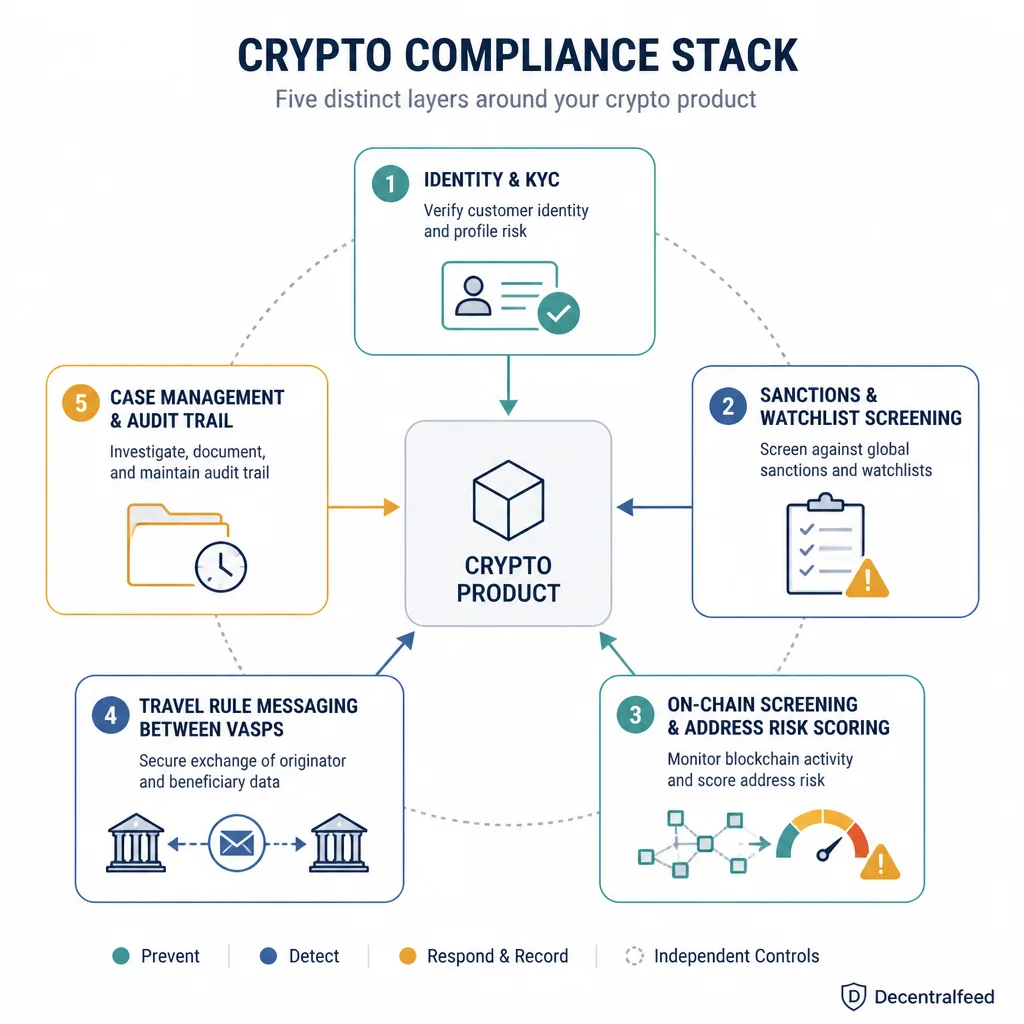

What the new compliance stack actually includes

A simple way to understand the stack is to ask what question each layer answers.

Identity and KYC: who the user is

KYC, and for business users KYB, is about identity. Who is this person or entity? Can you verify them? Are they who they claim to be? Depending on the flow, that may include document checks, liveness, beneficial ownership, and watchlist or PEP screening during onboarding.

This is the layer most people think of first. It is also the one teams most often overgeneralize. KYC is not all of compliance. It is identity assurance.

Sanctions and watchlist screening: who you should not serve

Sanctions screening asks a narrower but sharper question: is this person, entity, address, or jurisdiction prohibited or restricted under the sanctions regimes that matter to your business? In the US, OFAC is a key reference point.[^1]

That is different from general AML risk. A user can be fully identified and still be prohibited. An unidentified user may not be on a sanctions list at all.

On-chain screening and address risk scoring: what the wallet has touched

This is where blockchain analytics tools come in. Vendors such as Chainalysis, TRM Labs, and Elliptic typically focus on wallet screening, transaction tracing, entity attribution, and exposure monitoring.

The question here is not who the user is. It is what the wallet or transaction flow may be connected to: hacks, mixers, scams, darknet markets, sanctioned services, or other high-risk activity.

That sounds precise. It often is not. Address risk scoring is usually model-based and probabilistic. It reflects attribution logic, clustering assumptions, typology labels, and threshold choices. Useful, yes. Final verdict, no.

Travel Rule infrastructure: how regulated providers exchange required data

The Travel Rule is often described badly. It does not mean “collect full KYC on everyone because crypto is regulated now.”

At a high level, the FATF framework expects covered virtual asset service providers, or VASPs, to exchange required originator and beneficiary information when certain transfers occur between such entities.[^2] Local implementation varies. In the EU, the recast Transfer of Funds Regulation is one important anchor for crypto transfers.[^3]

This is as much an interoperability problem as a compliance one. Vendors such as Notabene and Sygna exist because regulated entities need a way to send that information securely and consistently.

Case management, alert review, and audit trails: the layer teams forget

This is the least glamorous layer and often the one that matters most.

A risk alert is not a compliance program. Someone has to review it, document the decision, escalate when needed, communicate with the user, and keep records. If your stack can detect but cannot decide, you have bought software, not compliance.

Many controls are not deterministic. They create queues, not answers.

These tools solve different problems, and teams often mix them up

KYC is not wallet screening

A fully verified user can still deposit funds from a hacked wallet. An anonymous wallet can have a clean on-chain history.

That is why KYC and wallet screening are complements, not substitutes. One identifies the person. The other assesses the funds flow.

Travel Rule compliance is not sanctions screening

The Travel Rule is about required data exchange between covered entities in certain transfer contexts.[^2] Sanctions screening is about identifying prohibited persons, entities, addresses, or regions.[^1]

They can appear in the same workflow, especially at exchanges, but they solve different regulatory problems. Treating them as interchangeable usually leads to either over-collection or under-control.

Risk scoring is probabilistic, not a verdict

This matters more than many teams realize.

Some controls are deterministic:

- exact name or list matches

- missing required documents

- simple geoblocking rules

- transfer counterparties confirmed as regulated entities in a Travel Rule workflow

Others are probabilistic:

- address risk scores

- suspicious behavior flags

- exposure tracing

- anomaly detection

Probabilistic systems are where false positives live. And false positives are not a side issue. They shape support burden, user trust, and review staffing.

A blocked alert is an operations workflow, not just an API response

Take a simple example.

Imagine a non-custodial app screens wallets before enabling swaps. A wallet gets flagged for exposure to a sanctioned service two hops away. What now? Auto-block? Manual review? Temporary restriction? Request more information? Escalate only above a value threshold?

The software cannot answer that for you. Policy does.

Compliance software does not remove judgment. It pushes judgment into thresholds, review queues, and exception handling.

Where compliance sits in the stack

Protocol neutrality does not settle interface obligations

This is one of the most misunderstood areas in crypto.

A smart contract protocol may be designed as neutral infrastructure. But users rarely interact with raw contracts. They interact with websites, apps, wallets, APIs, hosted services, and teams. That is where compliance pressure often lands.

So yes, protocol-level neutrality can be a meaningful design principle. But it does not automatically settle interface-level obligations.

Why custodial businesses usually face the heaviest requirements

Custody is still one of the clearest practical triggers for stronger controls.

If you control customer assets, move funds on behalf of users, or connect to banks and payment processors, expectations usually rise sharply. That often means full KYC or KYB, sanctions screening, transaction monitoring, Travel Rule workflows where applicable, case management, and recordkeeping.

A centralized exchange offering fiat deposits is the obvious example. It typically needs identity verification, sanctions controls, ongoing monitoring, and documented escalation procedures. That is not ideology. It is operational reality.

Why non-custodial wallets and DeFi front-ends sit in a greyer zone

Non-custodial products often live in a more contested area. Legal treatment may depend on jurisdiction, business model, interface behavior, fee capture, operational control, and commercial relationships.

That uncertainty cuts both ways. It does not mean these teams always need exchange-style KYC. It also does not mean “non-custodial” makes the issue disappear.

A realistic middle position is common: wallet screening, sanctions-related controls, geoblocking in some regions, and a lightweight incident review process, but not full retail onboarding for every user.

Why the same protocol can have very different interface policies

This explains a pattern many users notice but few articles explain well.

Two front-ends can point to the same underlying protocol and enforce very different rules. One may block certain jurisdictions and screen wallets. Another may be more permissive. The contracts are the same. The interface risk posture is not.

That is why builders should think in layers. The base protocol and the distribution layer are not always judged the same way by regulators, counterparties, or infrastructure providers.

The real tradeoffs: privacy, false positives, fragmentation, and UX

False positives punish good users and overload small teams

On-chain screening is powerful, but it is not magic. Attribution can be incomplete. Exposure can be indirect. Thresholds can be tuned too aggressively.

The result is familiar: legitimate users get blocked, support escalations pile up, and a small team starts making ad hoc decisions under pressure. Bad thresholds create bad product experiences.

Privacy costs rise quickly when controls stack up

Every added control collects more data, increases retention obligations, and expands breach surface area.

That matters especially for self-custody products. Users often choose them to avoid unnecessary data collection. If you stack KYC, wallet analytics, behavioral monitoring, and broad retention without a clear reason, you may solve one risk by creating three others.

“Global compliance” is mostly a slogan

The FATF provides a broad framework, but national implementation differs.[^2] The US, EU, UK, Singapore, Hong Kong, and others can diverge on scope, thresholds, licensing categories, and enforcement posture.

So “globally compliant” is usually marketing language, not a serious legal conclusion.

The hidden cost is not integration. It is exception handling

Most teams underestimate this.

The first demo makes compliance look like an API problem. The real burden appears later:

- setting thresholds

- reviewing alerts

- unblocking legitimate users

- documenting decisions

- updating policies

- training support and ops teams

- keeping records that can survive scrutiny

Integration is the easy part. Living with the consequences is harder.

Choose your architecture: a practical map

There is no universal stack. But there are recurring patterns.

| Architecture | Typical product fit | Common controls | UX/privacy cost | Ops burden | Best fit |

|---|---|---|---|---|---|

| Low-friction | Non-custodial app, DeFi front-end, interface-light product | Geoblocking where needed, sanctions-related wallet screening, basic policy controls, incident escalation | Low to medium | Low to medium | Products avoiding custody and trying to preserve self-custody UX |

| Middle-ground | Wallet, app with accounts, higher-value flows, stronger partner requirements | Selective KYC, sanctions screening, transaction monitoring, manual review workflows, case logging | Medium | Medium to high | Products with more user accounts, recurring counterparties, or higher banking/commercial pressure |

| High-control | Exchange, broker, custodian, fiat-connected platform | Full KYC/KYB, sanctions and PEP screening, transaction monitoring, Travel Rule tooling, continuous monitoring, audit trails | High | High | Regulated intermediaries and fiat-touching businesses |

Low-friction architecture

This is often the most proportionate setup for a genuinely non-custodial product.

A realistic example: a DeFi front-end may screen connected wallets for sanctions-related exposure, geoblock certain jurisdictions, restrict obvious high-risk interactions, and maintain an internal review policy for escalations. It may not require full KYC just to browse or connect a wallet.

This works best when the product avoids custody, avoids fiat, and keeps counterparty exposure limited.

Middle-ground architecture

This is where many teams end up.

If you have user accounts, higher-value flows, institutional counterparties, or business partners with stronger expectations, a purely light-touch approach can stop being credible. Selective KYC based on thresholds or risk triggers may make sense, depending on local rules and product design.

This model lives or dies on operational discipline. If alerts trigger manual review, you need owners, policies, and response times.

High-control architecture

If you custody funds, touch fiat, or regularly transfer assets between regulated counterparties, this is usually the baseline architecture.

A centralized exchange is the clearest example. It will often need onboarding checks, sanctions and PEP screening, transaction monitoring, suspicious activity escalation, and Travel Rule messaging with other covered entities where required.[^2][^3]

This is expensive. It is also often unavoidable.

A simple decision filter

If you want a shortcut, start here:

- Custody: Do you control user assets?

- Fiat rails: Do you connect to banks or payment processors?

- Counterparties: Do you regularly face regulated exchanges, institutions, or market makers?

- Jurisdictions: Where are users, operators, and entities located?

- Business customers: Do you need KYB and beneficial ownership checks?

- Review capacity: Can your team actually operate what it integrates?

The right stack is the lightest one that credibly covers those realities.

How to decide without overbuilding

Start with product reality, not ideology

“Decentralized” is not a compliance architecture. Neither is “just KYC everyone.”

Map the actual product flow. Where do users enter? Where do funds move? Who controls assets? Where do counterparties appear? Where does legal or commercial pressure attach?

That is the basis for design.

Ask what creates legal exposure

Heavy obligations often cluster around custody, transfer intermediation, fiat access, business clients, and regulated counterparties.

Sometimes the regulator is not the first pressure point. Sometimes it is the bank, payment processor, insurer, or auditor. Commercial survival can force stronger controls even before legal questions are fully settled.

Design for review and exceptions before scale forces it

A good early question is not “Which vendor should we buy?” It is “What happens when the vendor flags someone we do not want to lose?”

If you cannot answer that clearly, your architecture is incomplete.

Involve counsel early, but do not outsource product judgment

Counsel is necessary. But lawyers do not design onboarding friction, alert queues, or support workflows.

They can define risk boundaries. Product and operations still have to decide where controls appear, when friction is introduced, and how exceptions are handled without wrecking conversion or trust.

The practical takeaway

The best compliance stack is rarely the biggest one.

It is the one that fits your product, users, jurisdictions, and counterparties closely enough to reduce real risk while still being operable by the team that has to live with it. That usually means proportionate controls, not maximal ones.

A common builder mistake is mismatch. Some teams copy exchange-grade friction into products that do not need it. Others assume protocol neutrality removes all practical exposure. Both mistakes are expensive.

The better approach is simpler: identify the risk your product actually creates, then build the lightest stack that can handle it when the first real alert arrives.

FAQ

What is a crypto compliance stack?

A crypto compliance stack is the set of controls a product uses to manage legal, counterparty, and financial crime risk. It often includes KYC or KYB, sanctions screening, wallet screening, transaction monitoring, Travel Rule tooling, geoblocking, case management, and recordkeeping.

How is KYC different from wallet screening?

KYC answers who the user is. Wallet screening answers what risk the wallet or transaction flow may carry based on on-chain exposure. They solve different problems and are not substitutes.

Is sanctions screening the same as the Travel Rule?

No. Sanctions screening is about identifying prohibited or restricted persons, entities, addresses, or jurisdictions. The Travel Rule is about exchanging required sender and recipient information between covered regulated entities when certain crypto transfers occur, with local variation.

Do DeFi front-ends need compliance tools?

Sometimes. It depends on jurisdiction, business model, interface behavior, counterparties, and how much control or commercial involvement the team has. Even when protocol-level neutrality is part of the design, front-end operators may still choose or be expected to apply controls such as geoblocking or wallet screening.

When does the Travel Rule usually apply in crypto?

It generally becomes relevant when transfers occur between regulated crypto service providers, often called VASPs under FATF terminology, though scope and thresholds vary by jurisdiction. It does not mean every crypto transfer requires the same user data exchange.

What is address risk scoring in crypto?

Address risk scoring is a model-based assessment of a wallet’s potential exposure to sanctions, hacks, scams, mixers, darknet markets, or other high-risk activity. It is useful, but it is probabilistic rather than a final legal verdict.

Why are false positives such a big issue in on-chain screening?

Because they create real operational and product costs. A false positive can block a legitimate user, trigger support disputes, overwhelm a small review team, and damage trust. Good screening is not just about detection. It also depends on threshold design, manual review, and clear escalation policies.

What does a low-friction compliance architecture look like?

For some non-custodial or interface-light products, it may include sanctions-related wallet screening, geoblocking where needed, basic policy controls, and a lightweight incident review process. It is still a compliance design, just a narrower one.

What does a high-control setup include?

An exchange-style setup usually includes full KYC or KYB, sanctions and PEP screening, transaction monitoring, Travel Rule messaging where required, case management, suspicious activity escalation, and stronger recordkeeping and audit trails.

Can builders outsource compliance to vendors?

Only partly. Vendors can provide identity checks, blockchain analytics, or Travel Rule messaging, but the hard decisions still sit with the team. Thresholds, review policies, escalation paths, user communication, and jurisdiction-specific risk decisions remain internal responsibilities.

[^1]: Sanctions obligations and scope depend on jurisdiction, business model, and legal interpretation. OFAC is a major reference point for US sanctions compliance, but not the only one globally. [^2]: FATF sets a widely referenced international framework, but implementation varies by country and local law. [^3]: EU rules and guidance can evolve, so teams operating in Europe should verify current requirements against the latest legal text and counsel.