GENIUS Act Stablecoin Compliance in July 2026: What Changes for USDC, USDT, Users, and DeFi Wallets

If you use stablecoins regularly, the main risk right now is not that a new law suddenly makes your tokens disappear. It is that the path you rely on becomes less smooth.

Most users do not feel regulation directly. They feel it when exchanges change supported networks, issuers tighten redemption onboarding, wallet interfaces hide weaker routes, or liquidity thins on the chain where they hold funds.

One correction matters up front: July 18, 2026 is a regulatory watchpoint, not a confirmed cliff date for end users. The strongest primary-source reading is that the GENIUS Act takes effect on the earlier of January 18, 2027 or 120 days after final implementing regulations are issued.[^1] That makes July 18, 2026 better understood as the one-year rulemaking deadline, not the date when every USDC or USDT workflow changes overnight.[^1]

Still, July matters. Agencies are building the compliance framework now, and platforms often adjust early when they expect issuer status, AML rules, or U.S. offer-and-sale restrictions to matter later.[^1][^2] So the practical question is not, “Will stablecoins shut off this month?” It is: Which of my user flows could get more fragile first?

What actually changes

Why mid-July 2026 is a watchpoint, not a cliff

The OCC’s proposed rule says the GENIUS Act effective date is the earlier of 18 months after enactment on July 18, 2025, or 120 days after final regulations are issued.[^1] If final rules are not yet in place, the current backstop points to January 18, 2027.[^1]

So why care now?

Because July 18, 2026 is still the statutory deadline for agencies to issue implementing regulations, and rulemaking itself shapes platform behavior.[^1] Exchanges, issuers, custodians, and wallets do not wait until the last legal minute if they expect support policies, disclosures, or network availability to change.

What the law governs directly

The framework targets issuers and regulated intermediaries first, not ordinary token holders. The OCC proposal covers issuer licensing, reserve assets, redemption practices, reporting, audits, custody, and supervision.[^3] FinCEN’s April 2026 proposal would treat permitted payment stablecoin issuers as financial institutions under the Bank Secrecy Act, with AML/CFT, customer due diligence, sanctions compliance, and recordkeeping obligations.[^2]

FinCEN also says issuers would need the technical ability to block, freeze, or reject impermissible transactions.[^2] That is one reason compliance pressure is more likely to show up around redemption access, onboarding, and platform controls than around simple wallet possession.

What users are likely to feel

The user-facing impact is mostly downstream.

The OCC summary says digital asset service providers cannot offer or sell a payment stablecoin to a person in the United States unless the issuer is a permitted or qualifying foreign issuer under the Act.[^3] That gives exchanges and U.S.-facing interfaces a clear reason to review which tokens, pairs, and networks they support.

In practice, that can look like:

- a pair stays listed, but fewer networks remain enabled

- deposits stay open on one chain and close on another

- redemption access requires more onboarding

- wallet aggregators route around weaker pools

- a token stays visible, but the best exit path quietly worsens

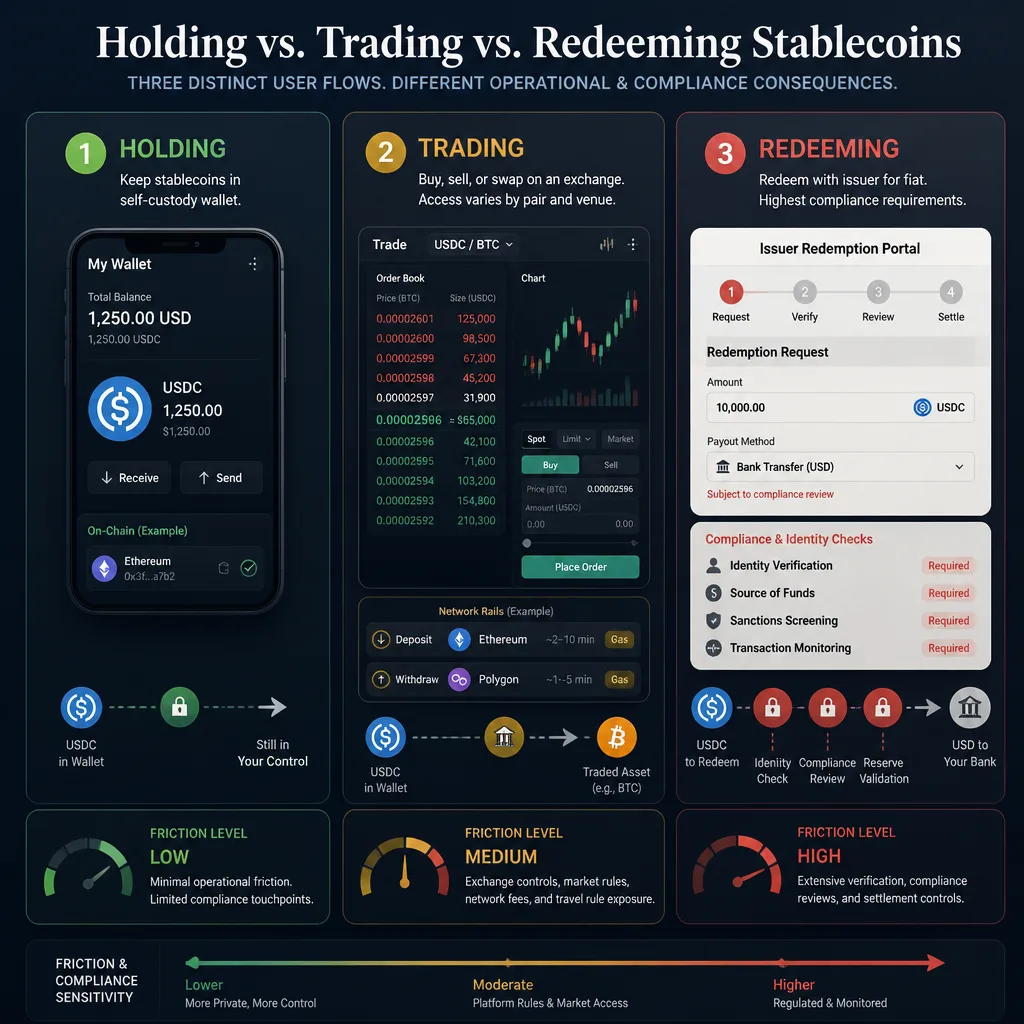

The distinction most users miss: holding, trading, and redeeming are different

This is the most useful mental model for July 2026.

Holding may remain possible even if support changes

Nothing in the current rulemaking suggests already-issued tokens become technically disabled overnight at the protocol level.[^1][^3] If you hold USDC or USDT in self-custody, the token can still sit in your wallet even if platform support narrows.

That does not mean usability stays the same.

Trading access can tighten before a full delisting

A platform does not need to delist a stablecoin to make it less useful. It can remove pairs, disable specific deposit networks, or restrict certain products for U.S. users.

Binance.US offers a good reminder of how venue-specific and network-specific support can be. Its June 18, 2026 SEI migration notice kept the SEI/USDT pair open while changing network handling for deposits and withdrawals.[^4] Different token, same operational lesson: support often changes by rail before it changes by ticker.

Redemption is the most compliance-sensitive flow

Redemption sits closest to the issuer, which makes it the place where AML, sanctions, eligibility, and reporting friction is most likely to appear first.[^2][^3]

Many users treat “I can trade it” and “I can redeem it” as the same thing. They are not. A stablecoin can remain tradable on an exchange while direct issuer redemption becomes harder, slower, or available to fewer users.

What may change for USDC users

Why USDC may be viewed more favorably by U.S. platforms

Circle has positioned USDC as aligned with the GENIUS Act path, calling the law “a clear path forward for USDC.”[^5] That is issuer messaging, not neutral proof. Still, it matters because platforms are usually more comfortable when an issuer is visibly leaning into the compliance framework.

Circle also says USDC is natively supported on 34 blockchain networks as of May 13, 2026.[^6] That breadth is useful, but it raises a practical question: which of those networks are actually supported by your exchange, wallet, or preferred off-ramp?

Likely friction points

The likely USDC story is not disappearance. It is selective tightening.

Possible friction points include:

- more explicit redemption eligibility checks

- more detailed network support notices from exchanges

- wider gaps between native USDC and lesser-used copies or wrapped versions

- venues standardizing around a smaller set of preferred USDC rails

There is already evidence of USDC-first market structure. Coinbase’s May 2026 Hyperliquid announcement described USDC as the preferred stablecoin underlying that market.[^7] That is not a universal market verdict, but it is a real example of liquidity and routing consolidating around USDC in a specific venue.

Real warning signs to watch this week

For USDC holders, the strongest warning signs are operational:

- your main exchange removes one of your deposit or withdrawal networks

- your wallet aggregator stops surfacing the route you normally use

- spreads widen sharply on your chain’s USDC pairs

- your preferred off-ramp supports a different USDC network than the one you hold

What may change for USDT users

Why U.S. treatment may differ from global liquidity

USDT remains globally important. But global depth and U.S. usability are not the same thing.

Tether’s January 2026 launch of USA₮, a federally regulated U.S.-market stablecoin issued by Anchorage Digital Bank, strongly suggests Tether sees a distinction between its global USD₮ footprint and a U.S.-specific compliant product path.[^8] That does not prove USD₮ becomes unusable for U.S. users. It does suggest U.S.-facing venues may eventually treat the two differently.

Likely pressure points

For USDT, the main U.S. pressure points are:

- more venue-by-venue variation than USDC

- fewer supported networks on regulated platforms

- selective pair reductions for U.S. customers

- a higher chance that interfaces prefer alternative dollar rails

At the same time, it would be wrong to frame USDT as instantly non-viable. Tether’s April 2026 announcement about freezing more than $344 million in USD₮ with OFAC and U.S. law enforcement shows active sanctions cooperation.[^9] That does not settle its long-term U.S. pathway, but it does weaken simplistic “USDT is out immediately” claims.

Where traders get caught

This is where traders make expensive mistakes.

A market can be deep globally and awkward locally. If your intended exit is a U.S.-facing exchange, a U.S. bank-linked off-ramp, or a wallet front end that filters routes, offshore USDT depth does not solve your problem.

The risk is not that USDT has no liquidity. The risk is that your version, on your chain, through your venue, has weaker liquidity than you assumed.

DeFi wallets and aggregators: where compliance shows up indirectly

Front-end restrictions versus on-chain token existence

This is where people often overstate and understate the risk at the same time.

There is not strong evidence yet that major wallets must hide USDC or USDT for U.S. users as of this month. But there is a plausible path for front ends to geofence, deprioritize, or reroute certain assets because compliance obligations sit upstream with issuers and platforms.[^2][^3]

So the better framing is conditional: the token may still exist on-chain, while the interface around it becomes less helpful.

Route selection and hidden fragility

If a wallet or aggregator changes route selection, users may first notice it as worse execution rather than a clear compliance warning.

That is why checking only the ticker is not enough. Check:

- which pool the route actually uses

- whether the route depends on a bridged asset

- whether price impact jumps at moderate size

- whether the “best route” disappears for U.S.-located sessions

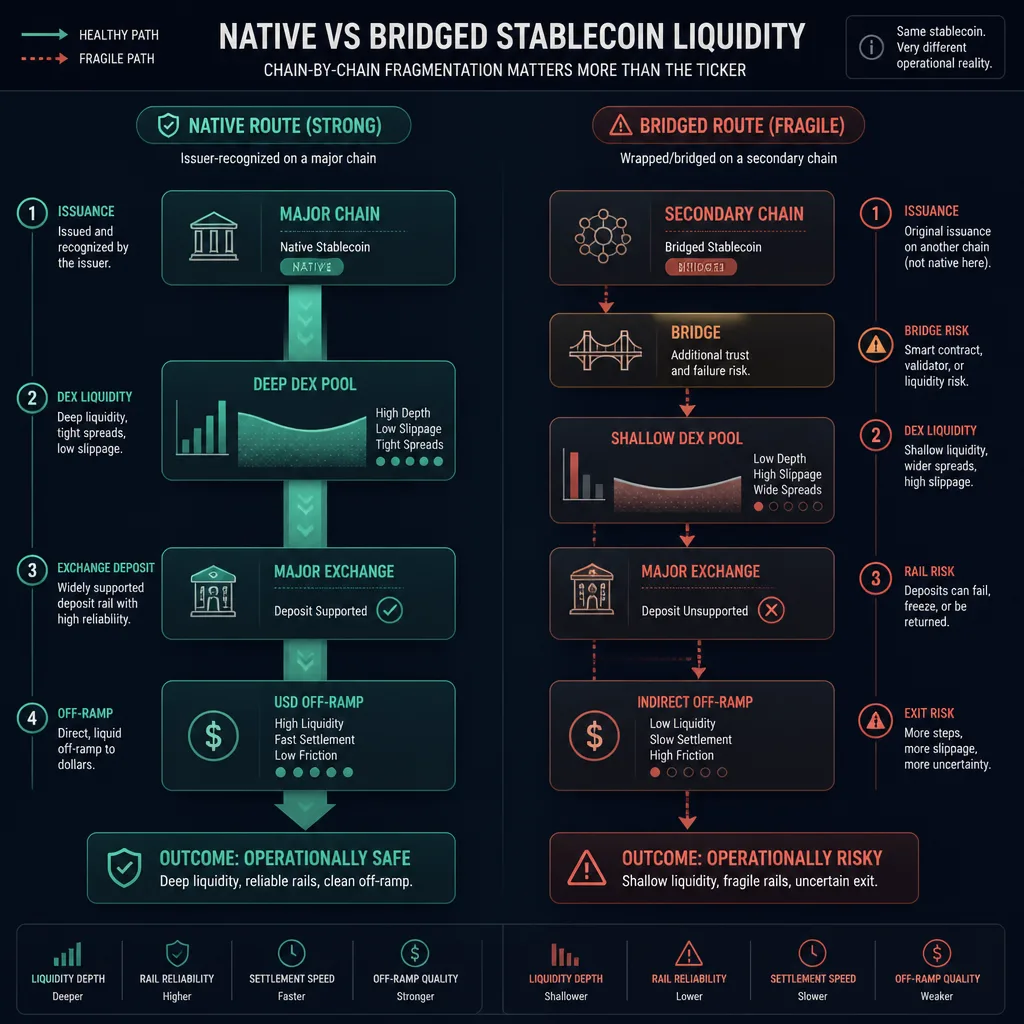

Why native versus bridged matters more now

Compliance pressure tends to reward clarity.

That usually makes native, issuer-recognized, venue-supported versions safer than obscure wrapped copies. The symbol may look identical. The liquidity profile often is not.

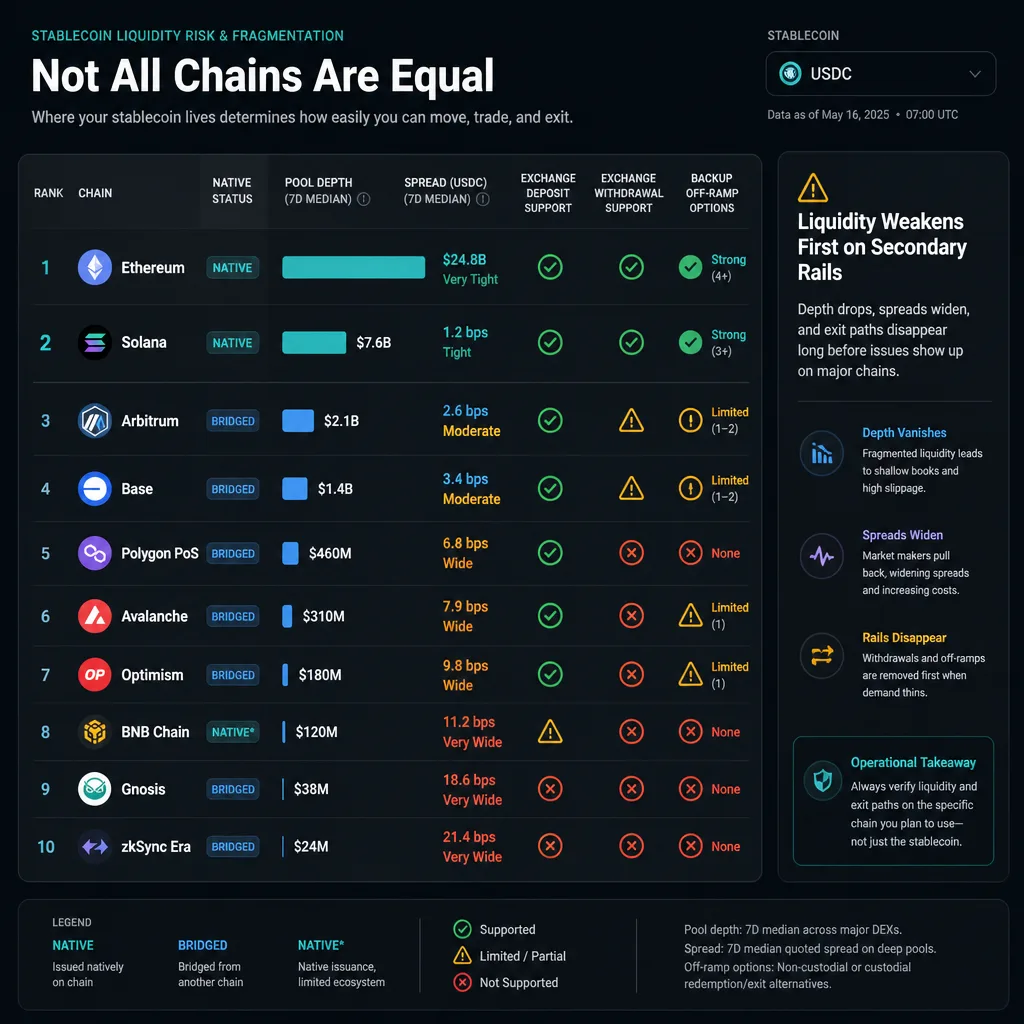

Chain-by-chain liquidity risk: the real problem is fragmentation

Why liquidity weakens first on secondary rails

Liquidity rarely disappears everywhere at once. It usually weakens first where support is already thin: smaller chains, secondary pools, wrapped versions, and exchange networks with lower demand.

That means fragmentation can hurt you before any formal restriction does.

How to identify the healthiest version of a stablecoin

A simple rule helps:

- Confirm the asset is native, not a random bridge representation.

- Check whether your main exchange supports deposits and withdrawals on that exact network.

- Look at live pool depth and spread before moving size.

- Make sure you have at least one non-DEX exit path.

If one of those fails, treat the position as less liquid than the ticker suggests.

When to consolidate and when not to

Consolidate if your funds are spread across low-depth chains, rarely used wrapped copies, or networks your main venues do not support.

Keep multi-chain balances only when you actively use those ecosystems and have tested exits on each one. “I might need it later” is usually not a good enough reason to leave size on weak rails.

What to check this week

Issuer status and official statements

Start with issuer posture.

For USDC, Circle is publicly presenting itself as aligned with the GENIUS Act pathway.[^5] For Tether, the more nuanced read is that USA₮ is the U.S.-specific compliance play while USD₮ remains global.[^8]

Exchange announcements

Do not assume support based on brand reputation. Check the notice pages of the exact venues you use.

The most important items are:

- supported deposit networks

- supported withdrawal networks

- pair availability for U.S. users

- any references to stablecoin policy, migration, or eligibility changes

Wallet and aggregator routing

Before moving size, run a small quote through the wallet or aggregator you actually use.

Compare:

- route visibility

- slippage

- output token version

- whether the route lands you in a token your exchange accepts

Pool depth and redemption alternatives

This is the unglamorous step that saves money.

If you cannot explain your exit path in one sentence, you probably do not really have one.

How to avoid getting stuck in illiquid pairs

Prefer native, venue-supported versions

If your exchange supports native USDC on one network and you are holding a wrapped lookalike elsewhere, the wrapped version is more likely to become inconvenient first.

Test the exit path before it matters

Do a small real transfer, not a mental simulation.

Send, deposit, swap, and withdraw once while conditions are normal. That is the cheapest way to discover unsupported networks and hidden friction.

Watch pair quality, not just ticker names

“USDT” and “USDC” are not enough information. You need to know the chain, contract version, pair depth, and whether your next venue supports that exact asset.

Keep a backup rail

One exchange, one chain, and one wallet route is not a robust setup anymore.

A practical arrangement is:

- one primary exchange off-ramp

- one backup exchange or broker

- one preferred native on-chain stablecoin route

- one tested alternative chain

What probably will not change overnight

Self-custody ownership of already-issued tokens

Holding a token in your own wallet is not the same as using a regulated service. Current rulemaking does not suggest self-custody ownership itself is what changes first.[^1][^3]

Protocol-level transfers

The more immediate compliance effects are tied to issuers, redemptions, and service providers, not to blockchains suddenly disabling transfers everywhere.[^2][^3]

Legal uncertainty is not the same as technical disablement

That is the broader lesson.

Regulatory implementation can be real and important without causing an overnight technical break. The first visible changes are more likely to be policy friction, liquidity fragmentation, and narrower supported pathways.

Conclusion

The cleanest way to think about GENIUS Act stablecoin compliance in July 2026 is this: the immediate risk is not token extinction. It is path degradation.

USDC and USDT may both remain important, but they are unlikely to be treated the same way across U.S.-facing exchanges, redemptions, and wallet interfaces. USDC currently appears better positioned from an issuer-and-platform perspective, while USDT may see more divergence between global liquidity and U.S. usability.[^5][^8]

That is why the best move this week is operational, not ideological. Check issuer posture. Check exchange network support. Check wallet routing. Check your actual exit path.

If you do that before you need to move size, most of the avoidable risk goes away.

FAQ

Is July 18, 2026 the main GENIUS Act stablecoin deadline users should care about?

Not exactly. July 18, 2026 appears to be the one-year rulemaking deadline, not the automatic date when all user-facing changes must happen. Based on the OCC’s proposed rule, the Act’s effective date is the earlier of 18 months after July 18, 2025, or 120 days after final implementing regulations are issued.[^1] If final rules are not yet in place, January 18, 2027 looks like the current backstop date.[^1]

Will USDC and USDT be affected the same way in the U.S.?

Probably not. USDC is generally positioned as more aligned with the U.S. compliance path, while USDT may face more venue-by-venue variation for U.S. users even if it remains globally liquid.[^5][^8] In practice, that may show up as different exchange support, redemption access, and network availability.

Do I need KYC just to hold or transfer stablecoins from a self-custody wallet?

Holding a token in self-custody is different from redeeming it with an issuer or using a regulated venue. The strongest near-term compliance friction is more likely to appear in redemption onboarding, exchange account requirements, and platform policies rather than in protocol-level ownership itself.[^2][^3]

What is most likely to change first for everyday users?

The earliest changes are likely to appear through platform decisions: supported trading pairs, deposit and withdrawal networks, redemption eligibility, disclosures, and wallet or aggregator route visibility.[^3] In practice, many users will feel compliance first as extra friction, not as a sudden technical shutdown.

Can I still hold a stablecoin if an exchange narrows support?

Usually yes, at least in the basic sense that the token can still exist in your wallet. But holding, trading, and redeeming are separate flows. A token can remain in self-custody while becoming harder to trade on certain venues or harder to redeem directly for dollars.[^2][^3]

Why does chain-by-chain liquidity matter so much now?

Because the real risk is fragmentation. Two tokens with the same ticker can have very different liquidity, redemption friendliness, and venue support depending on the chain and whether the asset is native or bridged. Users often get into trouble not because a stablecoin disappears, but because their specific version sits in a weak pool or unsupported network.

What should users check this week before moving size?

Check four things: the issuer’s current U.S. compliance pathway, exchange announcements on trading pairs and supported networks, whether your wallet or aggregator still routes through healthy pools, and your actual exit path if you need to cash out or rotate into another stablecoin quickly.[^3][^5][^8]

Does the GENIUS Act mean DeFi wallets must hide USDT or USDC?

Not necessarily. There is a plausible path for front ends to geofence, reroute, or deprioritize certain assets for U.S. users, but that should not be overstated without wallet-specific notices. The safer assumption is that interface behavior may change before the underlying token does.[^2][^3]

Is redemption more compliance-sensitive than trading?

Yes. Redemption typically sits closest to the issuer and regulated onboarding, which makes it more sensitive to AML, sanctions, eligibility, and reporting requirements.[^2][^3] Many users who can still trade a stablecoin on a venue may not have the same direct redemption access.

Could U.S.-facing exchanges keep support even if rules tighten?

Yes. Large venues may preserve some support by limiting functions, ring-fencing certain users, changing supported networks, or narrowing pairs instead of moving straight to full delistings. That is why venue-specific notices matter more than broad assumptions.[^3][^4]